Fintech #3 | Of floppies, caca CACs and commoditized banks

perpetual giveups r thr....

Not so long ago, I was working on my laptop, typing away a weighty tome on some long forgotten deal that would have changed the world. A nibling (or in this case, son of a very close friend) walks up, points to the Save button and asks me what it was. I told him, it’s the Save button. He says no, what is that thing in the icon.

He was of course, referring to the 3.5” floppy in the save button icon. Immediate facepalming ensued. This kid was born in a world where things you wanted literally wafted off the air into the phone/tablet/laptop. What did he know of CRT screens and CD drives and 5” floppies and hard drives? What would he make of dial up modem sounds?

When I showed him the floppy, his first question was why was it called a floppy? In my hand was a stupid plasticky coaster looking thing that apparently offers a meager 1.45MBs of space and decidedly doesn’t have any floppiness to it. It took a bit of doing to boot up my old Compaq Presario and show him what the ruddy thing did. Which was of course, a whole lot of clicky noises. While he was shaking his head in disbelief on how primitive we were, I was reminiscing about running around the hostel with hard drives in hand hunting for movies, and the abject terror one felt when the floppy started making clicky noises 20 seconds before one’s major project1 presentation. At the end of this, the kid says - “didn’t you have the internet?”. I was once again up memory lane, thinking of 2nd year Comp Science students hanging cat 5 cables on trees and jury rigging a network in the hostels using hubs (which were cheap, but murder on bandwidth) and a couple of switches (which were bloody expensive).

Kids can be cruel.

Anyway, here is a photo of the old friend that got me through engineering college. The cover was impossible to open unless you knew what you were doing (most people did not) which made the case an excellent hiding place for liquor and cigs.

Now, your reaction here may well be a WTF. I just wasted 2 mins of your time in this trip down memory lane. What does Mr Goyal’s need for climbing trees to bring internet to the unwashed and stinky (and sometimes crabs infested) masses at the student hostels at NIT Jalandhar have to do with Fintech?

Well, it’s another riff on the app-infra cycle. Here is a company you should look at - Plaid. I read somewhere about someone famous saying that APIs will eat software for breakfast. I think Plaid and Decentro and Unit will be quite full.

What that leaves me thinking about is this - are only two moats left - the efficiency of your burn (in terms of acquiring customers) and your ability to acquire banking relationships? And what happens when multiple “FintechCos” try to go after the same 70 million customers?

1. CAC approaches caca?

For most fintech companies that have crossed my desk, the question moving the investment decision most often is this - do they have a sustainable advantage to maintain a low CAC and hence a favourable LTV/CAC?

Almost everyone tries to show that they are superior on the LTV/CAC dynamic than the other guys. Now, I won’t go into long term assumptions underpinning LTV (given that only 4-5 unique use cases have been tackled so far in India) but the problem is that such models are usually super sensitive to long term transacting behaviour and churn (both of which are unknown initially). Now, whoever is most optimistic about this has the most dollars to spare on marketing - so everyone ends up competing at that level. You are going to be forced into that rat-race, literally.

Rat races, as we know, are lose-lose propositions. See, this is a game of hopefully optimized optimism. When everyone is going after the same pool of customers (70mn) via the same channel (Facebook, Google) with similar products - the company that is convinced that it will make most money off these guys in the long run will spend the most in acquiring them. Even if the optimism was misplaced, the damage has been done, the pitch has been queered, the barbarians are at the gates….. (ok fine, I’ll stop here). The most optimistic (and hence most spendy) company lost money. Everyone else lost customers. Lose-Lose.

Till about 2017 - the real differentiator for most was the product. Wallets, QR codes were genuinely better products. Once that became old, once these building blocks of the modern FintechCo became standardized, the key success factor changed to acquiring users. Think about it - how many financial products do you really use today? a bank account, a credit card, a debit card, some loans, some insurances, some investments, maybe a few wallets. Are these all not more-or-less standardized? So, how do you even build a profitable Neobank today? Even if you were going to sell financial products to folks who haven’t started shaving yet, there are multiple competitors converging there.

When anyone can sell some version of the same thing, acquiring customers becomes really, really hard. As more and more players vie for the same pool of users, CAC shoots up. So now, our FintechCos have to either live with a lower CAC/LTV ratio, or find a way to increase LTV (which is one of the reasons why the Neobank concept came about in the first place).

CAC quickly becomes caca.

2. Bundling is Profitable if it follows unbundling.

Imagine you run a restaurant (let’s say you are McDonalds). McD is tired of selling 20 Rs. burgers but it has heavy competition and would like to offer a differentiator. Let’s say they offer a debit card to loyal McD customers. What does this do? They (McD) get interchange revenue. If the customers are maintaining balances, they can get some of the float. They can charge an MDR on other payments, they can offer loans. Most importantly, they can offer really great deals to their customers which are valid on spends using that card at McD. Now, I have seen this playbook before - it was a former portfolio company called Loylty Rewardz2. However, I know for a fact that Bijai (the founder) had to scale a vertical cliff to make this happen.

Things are easier today.

But before that, you may want to ask me a question. Why do this and how does this tie in with CAC? Answer - To go to where the customers already are.

If you are a business like, say, Amazon, you already have the customers - so your CAC is low/negligible. You can generate more revenue. So both the denominator and the numerator in the LTV/CAC ratio move to give a better outcome.

Then this shift ties in with the evolution of fintech itself. Fintech 1.0 and Fintech 2.0 apps had to rely on their product. Every single connection had to be done by themselves. Same stuff done repeatedly, same hills climbed repeatedly because the infra did not exist.

Let’s take a look at the US market - Plaid is a good example of this infra building. They are an API company like Postman. They allow developers to connect their apps to people’s bank accounts. Now, if you are a fintech developer, you know how much simpler your life will be if you are able to rely on someone else who has done the work of integrating with the banks and maintaining those integrations.

Now that the infra is built - this is what the landscape elsewhere looks like:

So, in so many ways, the unbundling of banking is complete at a conceptual level. For each step / need, there is a separate company for it. Now what? It can’t keep getting broken down further into niche-er and niche-er things. Do I really want to work with 9 companies if I am trying to build a full-service business?

In my first post on Fintech, I had argued that risk-taking begets demand for lesser friction which begets demand for more risk-taking which begets demand for yet lesser friction. Today, the demand for lesser friction looks like a demand for bundling.

See, in the opinion of this observer, “product” itself has become a commodity (and it likely doesn’t matter how we slice and dice the definition of “product”). Now the battleground has shifted to audience. VC ecosystems have been playing the horizontal games for some time now. Right now is the era of vertical tech. And those companies will bundle everything they can under the sun. They have spent billions acquiring these customers. They have tons and tons of data on these customers. They will do whatever it takes to make sure that the hard fought for audience is not going anywhere else. Including banking.

3. AWSification of banking

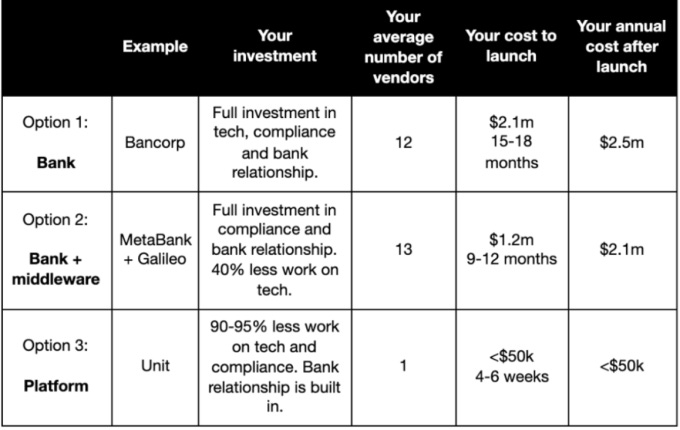

Unit is a great example of this bundling. They recently raised $18mn. The linked TechCrunch article has a nice table that I will copy and paste here.

That’s a substantial reduction - from 15-18 months to 1 month. While the cost may vary in India, I can totally vouch for the time it takes for setting up individual integrations. It is an absolute pain in the backside. And the less I speak about compliance, the better. Emails from bank compliance depts with phrases like “XYZ may be considered as a potential solution for ABC problem” are hard to parse. Are you asking me to do something or not?

This story too has played out before - AWS. Suddenly, all the investment going into servers and related hardware could go into other areas.

Closer home, while we have come a long, long way from the 2013 API opening by Yes Bank and RBL, I am not really aware of anything in this vein in India3. Would it not be awesome if I could build another Open in India using something like Unit? Decentro is the closest I have seen.

Now, I want to be proven wrong, but I don’t think this AWSification will happen in India anytime soon. See, the 2008 crash basically eviscerated faith in institutions in the US and European markets and severely weakened any arguments against innovation. Not so much in India. We may have differentiation based on UX in India but the banks hold too much power and regulatory benevolence to be shaken up like this.

4. Tracking History

Let me lay down a brief history of key enablers of fintech over the last decade:

Step 1 - Aadhaar and eKYC meant that you didn’t need to be present to verify your identity, and that the identity layer was largely standardised.

Step 2 - IMPS made payments instant. You could send as low as INR 5 and you could see it appear instantly in the other guy’s account.

Step 3 - UPI offered true interoperability. Yes, it’s built on top of IMPS in some ways. Its beauty is that it separated the addressing layer from the underlying account. So, I can have multiple accounts linked to one UPI ID and one account linked to multiple IDs. Authentication schemes became standardized. UPI pin is it-nothing else is really needed. Now, this opened up addressing layer offers some really interesting use cases like creating a unique UPI ID for individual invoices.

Step 4 - Sahmati (Account Aggregator Framework) was intended as the UPI equivalent for financial data. Consented flows from any financial information source to any financial information user. It was launched in 2016 but still, early days.

The next logical step here is for the regulator to say that the customers should be able to use any UX / front-end to access their bank accounts.

5. Desi Challenges

Most people think that I am a naysayer when I cast my doubts on the long term inability of Neobanks to make a dent in the banking business. I would be the first person to tell you how fervently I want to be proven wrong. I am rooting for the underdogs. You see, if we look at the banking partners of our intrepid fintech-onauts- we tend to see some usual suspects - Yes bank, IDFC, RBL, Equitas, PayTM, Kotak, Federal bank. Small guys whose interests are temporarily aligned with the Neobanks/FintechCos. If you are offering cards or specific SME accounts, sometimes ICICI will make a guest appearance. Why are SBI, HDFC, Axis and ICICI missing in the larger Fintech space?

At the heart of banking, there are 3 core layers:

Account Services Layer - open and manage the account. Now, this account can potentially be anything, not just a bank account. It can be an FD, a loan account, an insurance policy, a demat account. Yet unsolved.

Payments Layer - Money in and money out. Again broken into 3 more layers of addressing, authorisation and authentication. Solved by UPI

Data Layer - historical financial data for underwriting. Solved by Sahmati.

Solving the Account layer is what will allow AWSization of Fintech in India.

But that would commoditize the banks. Almost everything a bank does can potentially done by a third party. Except for the base layer i.e. the account. This is the design as mandated by the regulator. And for the minimal effort of squatting on this virgin territory which is ring-fenced by the regulator, banks get to stifle innovation the moment real competition comes up by simply closing the door. Sounds a bit like the mafia doesn’t it?

Most Neobanks are actually operating as prepaid accounts. The Neobank opens a large current account with the banks. Says - hey, I will run the accounting for the sub accounts, all of that will roll-up to the current account, and I will issue the prepaid cards against each sub-account. Now, upto INR 10,000, you need minimal KYC, so it’s pretty painless. Bank gets a zero cost liability that it can earn float on or lend out, and earn fat interchanges on prepaid cards. There is no threat to the bank yet.

The major differentiation today between Neobanks is their UX. So, Fi focuses on millennials, Fampay targets teens, Yelo has a pure vernacular interface and so on. Banks are not inclined to spend on this beyond a point so it costs them nothing to have a fat pool of capital sitting on their balance sheet while Neobanks and FintechCos gin up the business. Players like Open are exceptions (in that it opens an ICICI Current account) but technically, then they are really operating as a banking correspondent, enabling transactions through their platform. Again, slick UX but ultimate ownership still lies with the bank.

Now, the keen eyed among you will want to ask - if it’s only about deposits, why do we need a bank? I can technically put money in say - a gold ETF (another form of deposit) and keep spending against it using a prepaid card. Sure, but the deck is stacked against at nearly every step.

To issue a card you need a BIN (first 6 digits of your card number) and BINs are only issued to banks. If you are a Neobank and want independent access to NPCI - you are SOL because NPCI access is only provided to banks. And as owners of NPCI, banks decide who gets to come in.

Sure, you could argue regulation etc. but is there really a reason why I cannot use say PhonePe UX on an HDFC bank account? NiYo as another example gives me much cheaper forex rates. Why can’t I get the same on my HDFC account? After all, I can make UPI payments from 5000 different apps. Why should I not be able to do the same with the rest of my banking? Why should I be stuck with HDFC’s shitty IT? Technically, I would submit there is no reason for this. Demat accounts are also stores of negotiable instruments - and they are pretty much an open protocol. But the Regulator is unlikely to mandate this level of interoperability. You could argue that I should shift banks if I am so unhappy, but that is a specious argument at best.

The most often quoted bugbear is fraud. But wouldn’t more transparency make it easier for fraud to be detected? Fraud is almost always a pattern. In India, no one has a full view of fraudulent behaviour. Even the credit bureaus don’t talk among themselves. Openness is a benefit here, not a disadvantage.

A truly open model for the base layer will also solve the issue of size. Today, if I am riding in an Ola, I see 2 Rs. insurance from Acko. I am offered a Zest money loan at checkout in Amazon. All these are large companies talking to to other large companies. Size is an important driver of these relationships. Only the larger companies have the cash, the resources, the bandwidth and the patience to invest in such partnerships and make them successful. Banks have only so much bandwidth and a huge level of risk aversion so they again tend to partner with the largest firms. Another way to look at it is - think of how many kinds of financial profiles exist in India? Even if we took a million people in each cohort - we are talking about 1300 cohorts. How can a mass produced bank product work for 1300 different behaviours? but once I open up the account layer, there are potentially 1300 products that can be built and I can pick and choose what I want. Would that not be a veritable Cambrian explosion of creativity? But, for now, this door is closed.

I maintain that banks will not hesitate to copy what works. Nothing in banking is rocket science. Working with a FintechCo means that there is a per txn cost or a revshare4. Initially, it costs the bank almost nothing so they go along, but over time, as that revshare or per txn payment becomes meatier, the banks will pull that functionality in-house. It won’t be hard - APIs will already be built. Lessons from what works or doesn’t work in UX terms will already have been learnt. Regulatory issues will be easier to solve / get around given regulatory forbearance towards banks. The only things that I can see banks consistently outsourcing are customer acquisition (especially for loans), ATMs and analytics. For everything else, they will likely defend aggressively. And this will be enabled by the fact that banks’ access to capital is pretty much unlimited. Faced with existential threats, they will respond aggressively, including cutting off access to the account layer (as it recently did for a startup which was asked to find a new bank partner).

Now, I agree that there are enough and more arguments against what I am saying, and even for me it’s a deeply depressing PoV. Enough companies have achieved success in the fintech space being great intermediaries. But that’s the issue - intermediaries don’t control their destiny. Think of a Porter’s 5 forces style analysis for a FintechCo. Banks are substitutes, competition and (depending on your point of view) either customers or suppliers. Either way, there are only 35 of them in India - which means that whenever their finger comes onto the scale - it has a highly existential effect.

In the Matrix, Morpheus tells Neo(!)

“But they are the gatekeepers. They are guarding all the doors, they are holding all the keys which means that sooner or later, someone is going to have to fight them.”

He could well have been talking about desi banks.

As always, I look forward to hearing from you. If you liked this post, pls feel free to share this using the link below.

Usually, in 4 year engineering programs in India, you are expected to show that you have actually learned something by building a couple of apps or useful programs - it’s usually a requirement for graduation - the Major and the Minor Projects. Mostly it ends up being a large search exercise on GitHub trying to find something that you can talk about semi-intelligently and that you can clean out all comments out of. So, in a major project presentation, the prof knows you have lifted the code of the internet, and he is being magnanimous by not whipping you there and then, and you are shitting bricks because you know you have lifted the code off the internet and you are praying to all 330 million Indian gods that the prof doesn’t ask you any real question about whatever shit you are peddling that day as original work. In the interest of time, here are my responses to your most likely responses to this. No, Mine was original work. Yes, I am sure. Fuck you too.

Acquired by BillDesk

If you are aware of such startups in India, please let me know.

Otherwise, where is the non-linearity for the FintechCo?