VC#6 | Where are the next billion users?

Will the real gram vasis please stand up, and put one of those fingers, on each hand up...

A couple of months ago, I wrote a post about how, in the (likely) misplaced opinion of this observer, a large proportion of the recent run of Unicorns has been driven by FOMO. As of today, the funding raised by startups in the last 12 months exceeds funding raised in the previous comparable period by over $1.5bn.

We also have seen a run of IPOs like almost never before. Sure, markets are up and UPI mandates have made applying for IPOs a breeze, but I have not seen this level of activity since 2007.

Here is what scares the living daylights out of me. The current Nifty P/E is 28x. Last time Nifty P/E hit 28x, January 2008 had rolled around and Emaar MGF’s IPO was about to launch. Then, the proverbial shit hit the fan. A friend who was working on the IPO back then has been solely credited with the Jan 2008 crash (in my friend circle) and is often called upon in bull markets to work his magic and tank the markets a bit.

Then, there is a whole bunch of loss making internet companies making a beeline for the bourses. Loss making companies that should want to stay private (and hence out of scrutiny) are filing DRHPs like crazy. Why? What does Zomato know that it got listed and Swiggy doesn’t that it stayed private?

This question has had me scratching my head for almost 6 months now. I have a plausible answer, but it seems to be a little too devious for my liking.

This is likely the last couple of years where the internet companies can get listed on their growth metrics. Growth is plateauing and in some cases has stopped. So if we haven’t listed ourselves in the next 24 months, we aren’t going to be valued on a sales multiple and will likely have to generate actual cash flows (ugh!).

1. Old Data dies hard…

One of the earliest bits of data I used to track as a young VC investment manager at VenturEast was the number of phones in India and phone penetration. Over the years, somehow I have kept tracking that data. Blackberries died (RIP my trusty Curve 8300), Smartphones emerged and the phone penetration morphed into breakups of smartphones vs featurephones, 2G/3G/4G/5G usage, prepaid v/s postpaid breakup and so on.

Then I bought out a company called TSI, and I then started tracking the number of card users in India as well. Credit cards, Debit Cards, ATMs and so on.

Here is the thing - these numbers are quite well correlated. Postpaid phone usage seems to be the exclusive (ish) province of credit card holders. Here are the numbers:

Now, you will have to forgive me if my Postpaid data is not the most accurate (because govt doesn’t report this breakup) but I think its reasonably error free.

You may want to ask me why I made this hard left from FOMO induced IPOs to credit card and postpaid data users.

Here’s why - by most measures, these data points seem to represent the upper and lower bounds of the addressable customers for most internet B2C companies. For the purpose of this note, let’s try and see it as ~70mn users. This is the Total Addressable Market. Basically the population of Rajasthan or Madhya Pradesh or Tamil Nadu1.

All these billions of paper value - this is the underlying number of it all - 70 million people at the top of the pyramid.

2. … and new data gives little relief

Before we go any further, here are a few data points:

Zomato’s transacting base - ~10 mn users.

Swiggy MAU - ~15mn (I call bullshit on the 20mn number, but that’s just me)

# Amazon prime members in India - 10mn Users

Hotstar Subscriber base - ~20mn

Netflix Subscriber Base - ~3mn

PayTM MAU - ~150mn

Phonepe MAU - ~120mn

The keen eyed among you should really be calling me out right now. How am I claiming that there are only 70mn users as the addressable market when PayTM and Phonepe have double that number as MAUs?

Short Answer - habits, comfort and risk aversion.

3. Dissecting the User Base

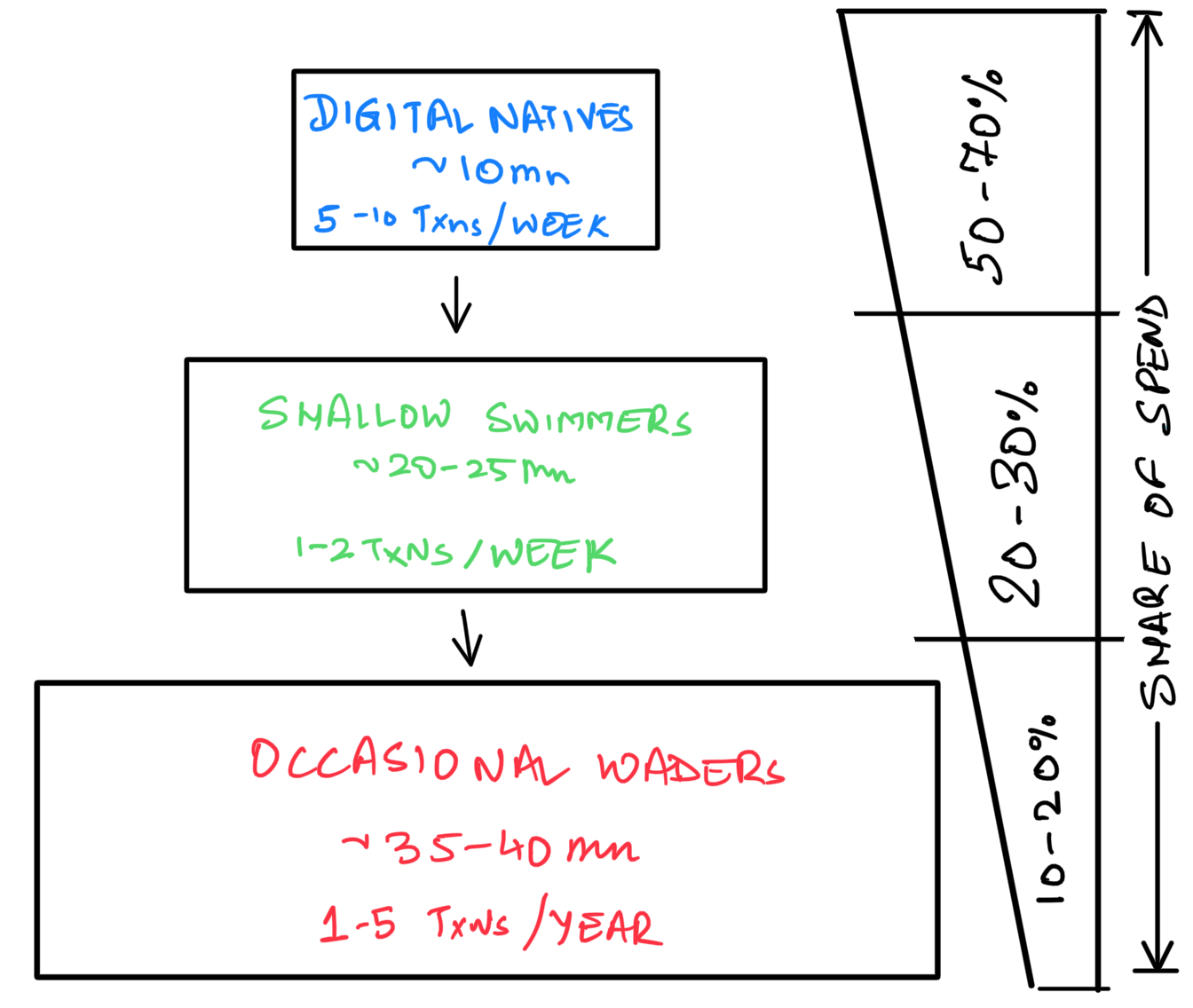

The 70mn active internet users can be broken down into roughly 3 buckets:

The Digital Natives: High disposable income - almost all the shopping gets done online. High propensity to spend - Online. Service quality matters most.

The Shallow Swimmers: Aspirers. comfortable transacting online but don’t necessarily have the cash or the tools to spend the cash online e.g. students. They know how, but are kept on a leash by mom and dad. Can be loyal but are extremely cost conscious.

The Occasional Waders: The person that gets pulled in on that really great mobile phone deal in the paper. They will do only this one deal, and thats it for the year (most likely). Extremely price conscious and risk averse. If there is a bad word of mouth about some e-commerce site - they are not going there.

4. GFT again

Now, lets go back to my assertion above:

This is likely the last couple of years where the internet companies can get listed on their growth metrics. Growth is plateauing and in some cases has stopped. So if we haven’t list in the next 24 months, we aren’t going to be valued on a sales multiple and will likely have to generate actual cash flows

This user base of 70mn has not really been growing of late. Sure, Covid had somthing to do with it - but it seems unlikely given that almost all the spending shifted online. If anything, it brought the divide into sharper relief. The inequality of income distribution has basically meant that while people may be doing better, they are not really moving between categories. The next 100-200 mn users from Tier 2/3 towns don’t really have the money to spend on anything beyond roti, kapda and makaan (Ok, maybe Jio prepaid too)

So, now, what’s to be done by the company that has a slowing growth, a capped user base and investors who are well aware of this plot? Going public is the only reasonable next course.

Pass the parcel to the retail investors. It’s hard to blame the exiting investors when they can hear this parcel ticking.

5. Context is everything

This doesn’t mean that the opportunity has ended. There is a huge opportunity, but its much more selective now. But this opportunity was not really possible without all that has gone before it.

You see, context needs to be created. The best example of this was Quiznos. For the longest time, Subway would not toast their subs. Then a company called Quiznos comes along, simply copies the entire business model, and as the sole differentiator, toasts the bread. That’s all. By the end of 2004, Subway was putting in ovens in all of its stores.

In the same vein, the opportunity that exists today is in B2C and vertical companies. Amazon and Flipkart created the context, but they have hit the ceiling. The future in India for these two involves a ton of grind. But vertical companies - doing one thing, and one thing very well are able to live off just the digital natives. In this world, a shoemaker called Bridlen can make shoes better than my Ferragamos and Berlutis for 25K and still be profitable. Fablestreet is able to make women’s clothes beating the Van Heusens and Allen Sollies of the world, BoAT is able to sell pretty decent quality wireless earbuds for INR 999. Aminu is able to build better products than MamaEarth and Wow Skincare.

The best part is that vertical focus on one thing allows for efficient value creation. It is not very capital intensive, the moats are easier to create, margins easier to defend and a significant advantage for the vertical leader.

Think about it, almost 40% of recent unicorns are vertical leaders.

As always, I look forward to hearing from you. If you liked this post, pls feel free to share this using the link below.

Trying to score points with the wife here by name-checking her state, bear with me.

Being a naysayer is a ticket to unpopularity - not that it's stopped you before.

So what's next, shorten these IPO Stocks?