Fintech #1 | Of Fintech, Wedges and Future.

Hello, Dear Reader.

I first wrote a comprehensive fintech report in 2015. Since then, I have been asked many times to write an update. Now, I have been avoiding this topic quite studiously. I didn’t want to fire up Powerpoint and make boxes all day - and this is a story that’s hard to tell without graphs and charts and 4 quadrant diagrams. Eventually inspiration (and downright harassment from friends - you know who you are) has trumped inertia.

Let’s Go.

1. There are only 3 value creation axes

Cheaper: I can charge you less rent as a gatekeeper or otherwise reduce transaction costs.

Faster: I can put your money to work quicker.

Better: My product genuinely offers better functionality or less hassle than others.

2. There are only two ways to make money in Finance

Modern Banking, as we understand it is about 600 years old. However, from the time that humans decided to use whatever we found scarce (and therefore of value) as a measure of wealth, there really have been only two ways to make money off money:

Become a more efficient middleman. Charge rent from transactions / information asymmetry as money flows from one person to another. We can earn an arbitrage spread or we can be paid for a service. We can be doing many things here - we can be reducing friction (UPI / payment networks), we can be providing infrastructure (Razorpay, Square), we can be reducing effort in acquiring customers(Credit Karma, BankBazaar) or we can simply be a safe (banks).

Take on financial risk aka skin in the game. We can Insure, we can Lend or we can Invest.

Any and all “Fintech”, by whatever categorisation we use, will fall into one of these broad buckets. B2B. B2C, SaaS, NIM, APR - all nuances/segmentations/positioning will eventually fall into these two buckets. Conceded that nuance is important but of late, my conversations seem to be going down rabbit holes of vanity metrics and irrelevant detail - it’s pointless.

It is important to set this context now. Keep this framework in the back of your mind as you read on.

Caveat: Almost all of what follows is now from an Indian context.

3. Where we are:

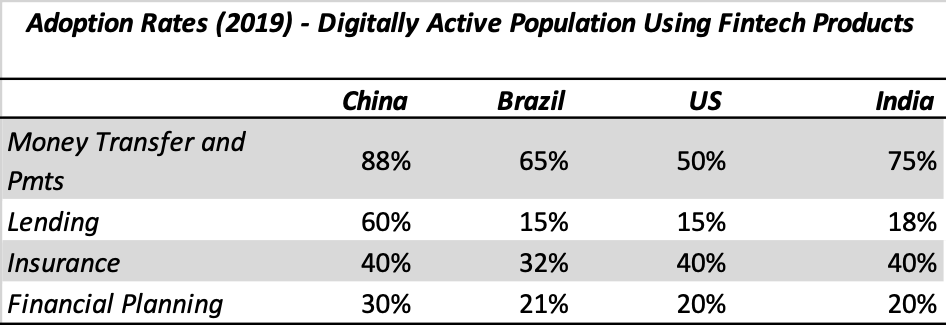

Let’s look at where we are today and compare India with China, Brazil, and US (as a reference market). The source for the chart below is Statista, but it’s paywalled so I wont bother with the sourcing.

Two key takeaways emerge:

India isn’t really that far behind other countries in most spaces except lending - but that seems to be more China doing too well rather than India doing badly.

Also, we see that world over, the penetrations among the Digitally Active Population are quite similar. That has likely to do with each country coming up with its own version of what became successful elsewhere in roughly the same period. It’s a version of the Kuznets curve.

4. Evolution of Fintech in India - A story of wedges.

We can divide the story of fintech in India rather neatly into 3 phases. Each had its own wedge(s) and relevance to the market. We have also alternated rather neatly between focusing on more efficient middlemen and focusing on taking on risk as ways to make money over the last 2 decades.

Perhaps it is a loop - risk-taking begets demand for lessened friction which enables risk taking which again demands yet lower friction, and so on….

Wedge 1 - Payments: Fintech 1.0 (if you will allow me the luxury) was based on disrupting payments. Credit/debit cards were recently launched, online frauds were rampant. No one really knew how to use these plastic pieces. The online wallet was secure, simple and elegant in its conception. POS machines that could be carried along in the delivery bag were a game-changer. Execution has been hard - but that’s OK. This falls under the more efficient middleman bucket.

Wedge 2 - Lending: Fintech 2.0 was about lending. B2B, B2C, B2D1 - nothing was spared. Digital loan pipelines became the norm, a lot of work was done on risk mitigation, underwriting, curating applicants for banks etc. As the India Stack and UPI matured, lending became easier and money poured in. We had some setbacks along the way with payday loans and the failure of P2P lending in India. Here is a measure of success - the time taken for loan underwriting has collapsed from 60+ days to 60 minutes. This falls in the taking risk bucket.

Wedge 3 - Platforms: Fintech 2.5 was about platforms and lowering friction. As payments and lending became crowded - we saw yet another hard left - platforms. Whoever dreamed up the idea of putting together a super-app was a genius. you already have the customer - why not offer him everything in one place. Of course, we have platforms like Cred who stretch the boundaries of what constitutes a business. Platforming has effectively married e-commerce with loans and payments. Another win for more efficient middlemen.

Wedge 4 - BNPL and Neobanks: Fintech 3.0 is about replacing bank products with jazzier alternatives. Same wine, newer, flashier, app-ier bottle. And it works. Square bought Afterpay for $29 billion earlier this year2. We have moved back into the take-risk model. BNPL and Neobanks are attracting the ability to take on risk by lowering friction. The jury is still out on how this works out in India.

Wedge 5 - Data accumulation and Underwriting: Fintech 3.0 has also seen another beast emerge - bookkeeping software. It’s the Zenefits model taken to its logical exreme in India. Give away a free bookkeeping software. Hoover up all the data, use it to underwrite, curate and otherwise push financial products with better risk management or better chances of closure (i.e. cut down on overhead). Once again - attracting the ability to take on risk by lowering friction.

All wedges aren’t all equal. I would argue that the incremental opportunity and potential for true innovation is dying because of the winner-take-all nature of the market. Most fintech work has been on the axes of cheaper or faster. I would like to see less incremental innovation and one truly Better fintech product come out of India.

5. What did we learn from two decades of Fintech-ing?

Attracting customers is largely (and certainly now) a function of how much money one can throw at it. e.g. On an INR 100 recharge, give INR 110 back (INR 10 cashback). You are set.

Attracting and keeping merchants on your platform is way, way harder. if they don’t get enough business or if they need to change behaviour beyond a point, no adoption will occur.

A “bank” that cannot lend (e.g. a payments bank) will not survive.

Vanity metrics are useless. Only healthy books with controlled NPAs and low overheads are rewarded. Focus on stress indicators is key as one scales up.

Making the relationship with the customers stickier is strongly correlated with success. Either you are in the most used 15 apps on a person’s phone or you might as well not exist.

No relationship in India is stickier than a customer’s with their bank. And while banks are called unimaginative and disparaged as out-of-sync lumbering elephants - they are watching closely at what works and what doesn’t. A lot of VC money is going into giving banks a lesson in what works and the banks will replicate. Original thought is tough. Copying is not.

Insurance is still a game of trust - sales still need a person. Online platforms are still a small part of the overall market.

Regulator is significantly behind the curve in Insurance. Simple things like preventive health check-ups are frowned upon.

Regulatory waffling, especially on fundamentals like KYC is a constant risk.

Uncomplicating things - easier to understand and transact - leads to success. Best example - Zerodha.

Stellar customer service is a key success factor.

Overvaluing startups doesn’t make sense. if you are managing risk properly, you are not going to grow beyond a given rate. Expecting non-linearity in fintech businesses is a direct precursor to significant heartbreak.

We still don’t know what exactly a Cred coin is worth.

6. Current Landscape - mapping the opportunity

Let’s try and map out the opportunities in Indian Fintech as it stands today. I will try and break it down into 4 quadrants. our axes are - Size of Opportunity, and relative Intensity of Competition. Kindly allow me to apologise for my handwriting. Here is what it looks like:

The upper right quadrant is where all the action is. It is also the place with highest amount of regulatory risk. Further, the government and the regulator have been quite active in mandating interoperable infrastructure. With volumes, costs fall. What that effectively means is that the exit opportunities get queered. The Q is almost always in favour of building - especially for banks where they own the customer, quite literally. Think about it - when was the last time we saw a bank acquiring a fintech player in India? However, the opportunities do allow for multiple winners here and for consolidation / bundling.

For my money, I would focus on the lower right quadrant of the chart. These companies are likely more reasonably valued, less crowded and have an ability to build more inevitability / stickiness in their business models. These are also areas where you need both tech, business model and execution chops. Sure, these segments need more capital and are less glamorous from a cash flow perspective, but at least the money is going into building an asset, not in customer acquisition. The value in these segments will not be headline-grabbing sexy, but investments here can easily deliver 5-10x returns. Put another way, is there a reason why any portfolio should reasonably be valued at more than 1.5x book?

I would not spend too much time on the left side of the chart today. These are either mature businesses or could-have-beens. These will likely provide acquisition targets to the right side of the chart.

7. What I would like to see more of

Finally, let’s take a look at some of the most attractive opportunities available today (in my opinion):

Access to Banking and Credit for Bottom of Pyramid: I started my career in 2008. Since then, this has been one of the most talked about and yet, most underserved segment of Fintech. Closest we have come are MFIs and Self Help Groups. With #2 above, plays in this area can be a huge, long term successes. However, this requires deep pockets to execute. Of all the business models possible today, this one is tough because it still needs significant IRL presence. You need field force, trainers and evangelists to convince the historically excluded population that they need to come into the fold of organized credit. It is not an easy trust gap to bridge. With advances in digital underwriting pipes and credit scoring models, one hopes that there will be products for lending to SEC 2/3 or blue collar workers. Access to retail credit is heavily skewed. ~10% of households account for ~80% of formal credit in India. Of course, I am happy to recognize my disdain for funding iPhone 19 purchase for kids not yet out of school. Might as well provide financing to someone who really needs it.

Cash to Digital Interface: The most successful “Killer App” in India would be a great, frictionless Cash to Digital Interface. All the spending we do online is ultimately tied to a bank account. 60% of our economy is cash based. An easy solution is transit cards that evolve into payment networks (like SG’s NETS and HK’ octopus cards). India has 60+ public transport networks, ~25 of them in smart cities. The opportunity is quite obvious. However, this needs massive capex in seeding readers/cards and managing the regulatory landscape. It hasn’t happened yet, but I hope to one day have my garage access card, office access card and cash wallet on a single card like in HK.

SME Lending: ~$800bn market, almost 70% of which is informal. Some progress has been made in cash flow based lending but it’s not enough. I have a lot of hope from OCEN which should let discovery (and hence servicing) of historically underserved segments. It is quite literally an OCEaN of opportunity if done right.

Insurance: India is one of the largest markets in the world for Life and Motor insurance. We have the lowest penetration for almost all other kinds of insurance (except health, where govt schemes have had massive impact over the last couple years). There are a few yet-untackled problems here - Better underwriting models, ability to customize insurance basis needs, great field force / agent management software, frictionless claims. Companies like Digit and Kenko3 are doing a lot but we need many, many more of such enterprises - which challenge the status quo and force the regulator to enact forward looking, enabling policies. It is hardly smart if a cancer policy cannot come with a free PET scan because regulator thinks it is inducement.

Compliance / Virtual CFO and CS: Lastly, while this view of mine may be extremely unpopular, I think this segment done right will create a few unicorns. It is often a hidden problem, simmering under the surface. Almost every company falls afoul of Compliance / regulatory and tax filings unless they are spending a lot of money on professional advice. But these are, highly rules driven and mechanical processes. Why can’t these be automated?

As always, pls feel free to reach out with your views / observations / corrections.

Business to Dog. https://lendingusa.com/borrowers/pet-retail/

if you can, please read the investor presentation. It’s a masterclass in succinctly and clearly communicating and highlighting the synergies and drivers for value accretion in M&A.

I missed investing in Kenko last year. It will likely be one of the most expensive missed opportunities for me. Perhaps I should also maintain a Bessemer like anti-portfolio.