VC#12 - What's in a Valuation anyway?

From state secrets to signalling mechanism.

Hello there. How have you been?

Last week has been a bit of a pain in the behind. The Missus and I both got Covid. We hid for quite some time, but we couldn’t outrun it in the end.

As I lay on the bed making plans of how I would slowly castrate the jackass who caused us both such misery (with a rusty, blunt spoon) and other pointless fantasies, Mint came in with the goods:

“Five years after making its biggest bet in India’s e-commerce market, Jack Ma-led Alibaba and Ant Financials have exited Paytm E-commerce Pvt. Ltd, the parent entity of Paytm Mall.

Paytm E-commerce bought back the entire stake of Alibaba (28.34%) and Antfin (Netherlands) Holding (14.98%), a total of 43.32%, for ₹42 crore, according to the company’s filings.

This values the company at a mere ₹100 crore, plunging from $3 billion, the valuation the Vijay Shekhar Sharma-led company fetched in its last fundraising that was in 2020”

Now, PayTM has had its swings in fortune but this one is quite extreme.

A long time ago, I was looking at a deal where we were looking to invest in One97 (PayTM’s Parent entity at the time). I spent almost 6 months on it and it was some of the best work I have ever done. It was a secondary sale and while the valuation was a bit rich, it was by no means out of whack for the growth on offer. Ultimately, one of the Partners at the fund1 asked me to drop the deal. As the only person on the team with any understanding of the mobile revolution2, I tried to cajole the leadership, 3 partners agreed (after a 2 hour marathon discussion) that the deal made sense. This gentleman did not. The people who did that deal instead of us made 40x returns. Think about it, 40 times money!! And real returns, not paper stuff.

So I was right. But only for a while. Given the meltdown in valuations, the deal ultimately would have made no money had it been held till now3. So this Partner was also right. As it turns out - on the karmic wheel of valuations, sense and sensibility are cyclical. But valuations are signals and over the last two years have effectively been weaponized.

Let’s get to it.

1. Bonfires of Dreams

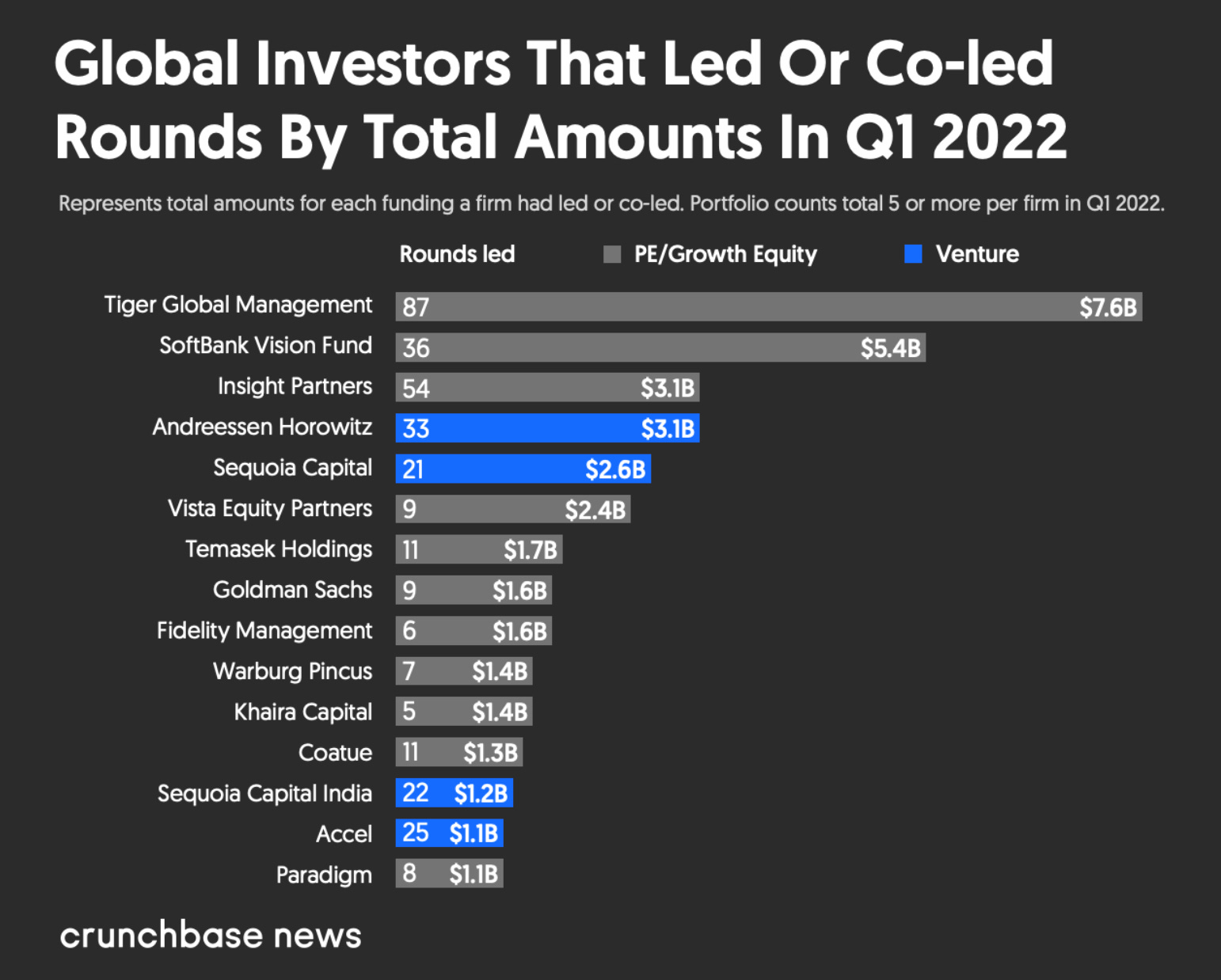

I have written a little about Hedge Fund and Cross-Over investing (“HFC”) earlier (especially Tiger). That post is here. There are some more great resources in the additional reads section below.

Now, given whatever has been happening in the markets over the last few weeks, it is clear that there will be many more clothes-less emperors made apparent in the next few months. The only way to describe the last couple of years from a private markets standpoint is MINDLESS, CHAOTIC FOMO. And some of the more interesting busts will come from the HFC world.

Tiger pioneered something called Founder Friendly Capital (FFC) deployed at crazy velocity. Briefly, they outsource high level diligence, pay above market prices and generally stay out of the entrepreneur’s way. They also move fast to deploy as much as fast they can. Or, to quote Packy McCormic, when “Tiger wants to win a deal, it doesn’t fuck around”.

Of course, now Tiger has been hit by a $17 bn loss. Think about it. Tiger was the most active investor in 2021. Even as of Q1 of 2022, it was throwing more money out than anyone else (even Softbank, and that’s saying something).

OK.

Now, Tiger is by no means alone in this. SWFs, public market only investors, pension funds, all have joined in this party. What’s going on here? Let’s take a bit of a meandering drive to figure this one out.

2. Valuation as a Signalling Mechanism

Sometimes I feel like I come from a bygone era of Private Markets.

When I used to look up companies, you could not work out the valuation. You would get funds invested or stake but not both in the press releases. Valuations were closely guarded state secrets. We used to guard them because we did all the work and the valuations used to help us negotiate the next investment. There is no point in spending 6 months working on a deal if someone can simply offer 25% more than what you have and snatch the deal away from you.

Today, the first number you see is the valuation in each and every press release. What happened?

HFC happened. FFC happened. Tiger Global happened.

See, the price and valuation are signals and anchors. The valuation in the press release becomes an anchor, a starting point for the next conversation, for the next round. When it is time to pawn off loss-making companies (with no business model) to public investors, that is the starting point of the conversation for the IPO (Here’s looking at you, OYO).

3. Mark-ups - Games of Skill or Games of Greater Fools?

You will likely notice another trend. Some people tend to invest together. Here is that playbook:

Take a company in a good sector with apparent demand.

Put some money in it at a crazy valuation.

Then, find a few friends and put more money at a crazier valuation.

Go to step 3, rinse, repeat.

Benefits? Everyone gets to mark up their books at the last crazy valuation. Use those unrealized results to raise the next fund. AUMs rise, management fee goes through the roof. And until a few months ago, you could even turn the paper gains into real ones by IPO / OFS route. Funnily enough, this unrealized stuff helps prop up shops which if marked honestly would be shut down yesterday. From Bloomberg:

“Coleman’s Tiger Global Management saw its hedge fund plunge 34% in the first three months of the year, while Laffont’s Coatue Management and Halvorsen’s Viking Global Investors fell 9.9% and 7.9%, respectively. Another Tiger offshoot, D1 Capital Partners, sank 16% in that time. Unusually, Tiger Global and D1 said they wrote down some of their private investments alongside their public market losses.”

“D1’s hedge fund was up 26% in 2021, powered by a 70% gain in its private holdings as its public portfolio fell 8%, while at Tiger Global, the hedge fund’s 7% decline last year compared with a 54% rise in its Private Investment Partners funds.”

“But the private holdings could prove problematic if investors want to leave and the closely held companies are marked down; Coatue recently told exiting investors they won’t get back their cash that is invested in privates.”

Tiger Global’s managers “adjusted valuations down” for the fund’s private investments to account for pressure on their public-market peers, they said in the letter to clients last week. The fund owns shares of private companies including ByteDance, Stripe, Checkout and Databricks. It’s unclear what those markdowns mean for Tiger Global’s venture business, which had assets of $65 billion at year’s end.”

Ouch!!

Here is a great example from Ranjan Roy’s blog:

Laceworks is a cybersecurity company.

2015 - Laceworks raises $8mn in series A from Sutter Hill. As traditional a VC firm as it comes.

2018 - Laceworks raises $24mn in Series B from Webb, Sutter Hill, Liberty Global, Alumni Ventures and so on. So far, so good.

2019 - it raises another $42mn from the same bunch as follow-on money, pretty normal trajectory so far.

Jan 2021 - Series C of $525mn Tiger, Dragoneer, D1, Coatue, Altimeter.

Nov 2021 - $1.3 billion. All of the above + Morgan Stanley and Templeton.

So what we had was a pretty normal, good company growing well till 2019. then Jan 21 rolls around and crazy season began. Laceworks is now worth $8.3 billion. Funny thing? In less than a year, Tiger and everyone else from then Jan round 5xed their January money with their own money. Ajay Relan would have called bullshit and chased me with a broom had I come up with such a strategy.

But then, what do I know? Tiger took this result to town and announced a $12.7 bn growth fund in March of 2022, raised in less than 4 months.

November 21 + 4 months = March 22. Sometimes basic arithmetic can give insights and context.

4. Inflated Valuations = Inflatable Lifeboats?

Now, let’s bring all of this together. I don’t think anyone at Tiger or its ilk is not aware that these valuations are all on paper. But ever rising crazy valuations persist. What’s going on?

See, no one involved is interested in seeing any markdowns. No VC/ Hedge fund wants a markdown, No LP wants a markdown. No Start-up wants a markdown. This creates an environment where as long as we say all is well, we can pretend all is well. Stripe is a great example. When Fidelity marked down Stripe by 9%, there was much gnashing of teeth and rending of clothes. Here’s the funny bit - Paypal and Square are down 50% each. How is Stripe, a much smaller, decidedly less mature business down only 9%? Simply because it is not listed? That’s some insulation.

Inflated private valuations should not hold. Right? All these perfectly priced valuations have already baked in perfect execution, perfect growth, perfect market exploitation. But what happens when growth slows and cash runs out? When these companies need to go and raise more money, there will be an inevitable pricing down. Right?

Answer - It will happen, but we do not know when and who. Someone has to blink first and bring this whole edifice crashing down. And no one wants to be the one to do that.

in 2015, Fidelity marking down companies was a huge deal. In 2022, Fidelity marking down Stripe and Instakart is a huge deal. Perhaps Fidelity is the Grim Reaper we need to bring sanity in.

After all, markups are not returns.

Additional Reads:

My post on Hedge Funds in Venture Capital here.

The Generalist’s Deep Dive into Tiger.

Abraham Thomas has written about the capital cycle far more concisely than I can here. He calls it the Minksy Moment. Apt description.

Ranjan Roy has a crazy insane funny take on Softbank, comparing it with the Vietnamese Dong here.

Housekeeping

As always, I look forward to hearing from you. If you liked this post, pls feel free to share this or subscribe to this newsletter using the links below. I try to write a 1000-2000 word essay once every two weeks.

This gentleman swore by US MBAs telling us poor IIM types how we are just useless and our education is not up to standards. Then one day he asks his shiny HBS interns to come in on a Saturday only to be told that the interns had a life and that the interns would see him on Monday. 4 poor IIM Types could not help but laugh. After this the jabs on IIM quality stopped.

The same Partner called my Galaxy S3 a toy and a passing fad. I hope he is still trying to install Tinder on his Blackberry.

Of Course, no one would have held it till now but it’s a moot point.