Today’s post is a little different. It is less a view on things and more of an introspection.

A very large proportion of the subscribers on this blog are people from VC/PE firms. While I would like to consider it a badge of honour, what really is going on likely is that us investment types greedily get ourselves on any and all mailing lists on the off chance that we might get something useful out of it. I know I do. Give me the transmission. It might be full of noise 99% of the time but I am betting I can make use of the signal that comes through 1% of the time.

A good place to start today’s ramblings would be Oaktree Capital’s Sea Change memo. Howard Marks is a Mount Rushmore figure. Perhaps it becomes us to pay attention to what he is saying. He makes a few interesting points in this memo but the most important ones are: 1) Success is highly correlated with intelligently navigating the risk/reward dynamic; 2) declining interest rate environments were perhaps the single most important tailwinds for returns; and 3) because safe investments (think 30 year T-bills) were delivering such abysmal returns, investors piled on in riskier assets thus increasing the systemic risks and throwing the risk reward dynamics completely out of whack. It should go in the must reads of investing, along with Maboussin’s Frontiers of Finance notes. Coase’s research paper and the Nomad Partnership Letters.

A. Where we are:

Looking at what all is happening in the business of managing money, all kinds of insane AI announcements (and more importantly, AI capabilities) and the macro environment, I am pretty sure that this time, things are a fair bit different - enough to make me feel like we are headed into the great unknown.

Here are 3 key trends that I think summarize the most important changes in the last 2 years:

The evolution of Venture capital (and Private Equity to a slightly lesser extent) to a high frequency exercise instead of being an inherently cautious, low frequency game.

Data science being amplified by AI to change the way the investment process works; and

Systemically lower returns going forward.

A1. Frequency of VC:

If you are reading the financial papers, you know that everyone and their uncle are starting VC funds. Why that is happening is a different conversation (and one we briefly visit later) but here is what I want to say - more dollars in the VC industry has led to an increase in competition. One of the ways that VCs now compete is to simply move faster1. Now, moving faster can take a few different shapes:

Invest in promising entrepreneurs earlier: A great and very recent example is colleagues reaching out to OpenAI engineers just as they are hitting their 4 year vesting thresholds. Investors are climbing over each other to attend conferences like KubeCon and ICML.

Multi/Late stage funds are targeting upstream investments: Greylock and Bain are great examples of firms which have launched high quality programs to work with entrepreneurs at earlier stages.

Funds speeding up diligence processes: Tiger is a great example of this. Get a term sheet in earlier and you might just cut off rivals at their knees.

To me, it is a direct parallel to high frequency trading. Funds that get to a trade first generally outperform others making the same trade later, or may even squeeze everyone else out. How that plays out in VC is that there is generally one VC that gets the shareholding and the terms that it wants, often at the expense of other funds. However, just because you became first to bid does not mean that you get the deal.

To my mind, the jury is still out on how to increase the probability of winning the deal. Firms that continue to remain profitable franchises will have a solid answer to it.

Others will become thin frontend wrappers on top of commoditized capital.

A2. Rise, fall, rise of Data Science - and a bit of AI:

In the previous section, I made a point about going earlier stage in the search of returns. The question then becomes one of discovery. How do you find the right early stage investments. Funds typically have vast amounts of data, even if they may not realize it. think about it, over my career alone, I have seen approx. 350 deals a year. That works out to ~6,000 transactions / efforts I have concrete, detailed data on. If one could use data science2 to tease out the signal out of this raw data - it represents a treasure trove.

And increasingly, others have been coming to the same conclusion. Smarter, more technically sophisticated shops have been using data science to discover interesting companies weeks if not months ahead of more mainstream investors. Hummingbird Ventures is one of the best VC firms you have never heard of that does this.

A very basic version of this looks like tracking github repositories, # of collaborators and so on. However, as these metrics are increasingly being gamed, the sophistication is shifting.

So today, I use slack / discord conversations and analyze them to figure out the relative “heat” of a deal. One of the more interesting thing one of my analysts has been doing is using GPT to analyze Hacker News and ProductHunt, at scale.

However, the place where I have found AI to be a huge amplifier has been in due diligence. A lot of data crunching like cohort analysis and building projections can be outsourced to AI tools. Sure, I have to do sanity checks on this but these tools have reduced the drudgery3 of our workflow by about 80%. Another huge use has been to automatically transcribe and summarize expert calls and use that as a way to refine our automated discovery efforts. What that allows someone like me to do is to focus on the parts of the deal where a human touch of a senior professional is needed, not the mechanics.

Needless to say, the discussions my team and I have these days are a lot less about excel modelling and a lot more about what those models mean.

So if you are a VC/PE professional, you ignore these tools at your own peril.

When I graduated from B school - great google-fu was a key differentiator. In the next decade, it will be AI tools.

A3. Systemically lower returns:

So, let’s talk about the Noah’s flood of VC dollars we see these days.

As a whole, I think the whole 2016-2022 period was one of over-raising. High returns were promised (never mind that the returns from with much smaller funds and much smaller # of funds). Today, we find ourselves in a situation where we are:

Competing for a small number of high quality deals (hence the rise of the party round).

…in a higher interest environment which is crushing returns (although 2023 seemed to have not been as bad)…

…even as larger pools of capital are having to compete on sensible dealmaking due to increased competition.

This translates into higher valuations, lower ownerships, far less stringent terms on founder behaviour and hence, even worse returns.

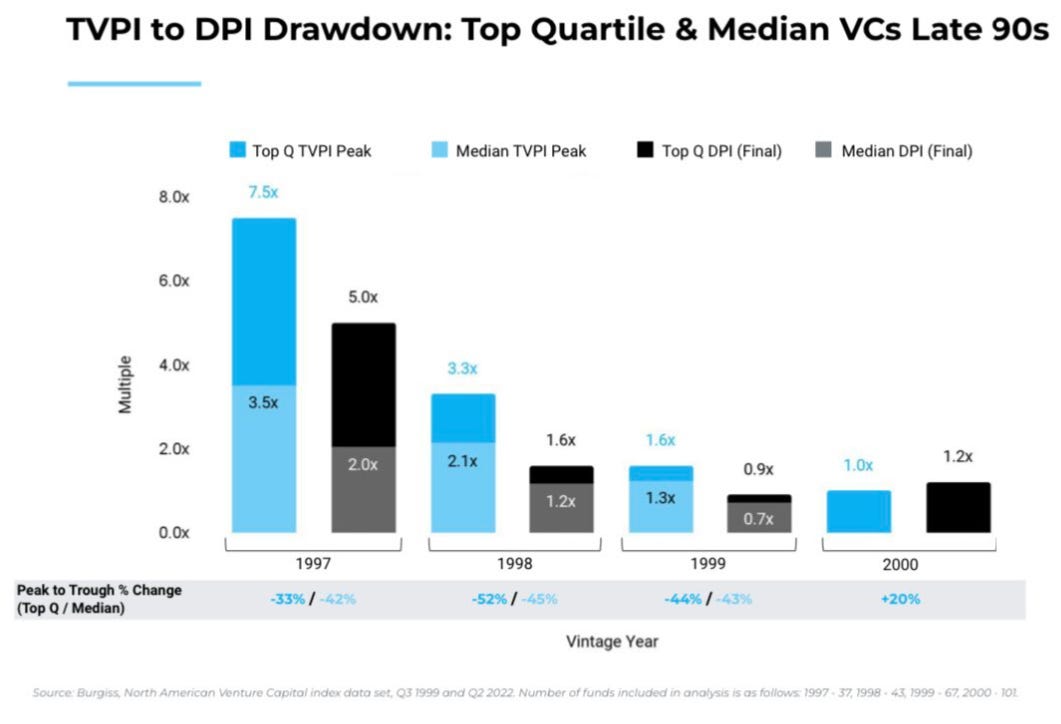

Predictably, both DPI and TVPI4 are lower. In fact, per an analysis by Cambridge associates, breaking 2x DPI is a rare, rare event.

So lets see what that means for a hypothetical $500mn fund trying to generate 3x:

Assuming 2/20 - approx 20% goes into the fee pool over a 10 year period. So the investable capital is only about $400mn5.

Assuming 1:1 investment to reserves ratio, we use $200mn to make the initial investments and keep the remaining $200mn in reserves to invest in the winners.

Now, let’s assume we do $10mn deals at $40mn pre-money6. This means that with our initial $200mn, we can make 20 investments at an average shareholding of 20%.

Now, going back to LP returns, the initial $400mn of capital now needs to return $1.75 bn in gross proceeds to get $1.5bn in net proceeds to LPs7. We need to make ~5x on the $400mn. In simpler terms, if the fund owns 10% at exit (assuming subsequent rounds’ dilution), we need our companies to be worth $17.5bn at exit so we can get $1.75bn in the fund. And real DPI is much lower (as seen above).

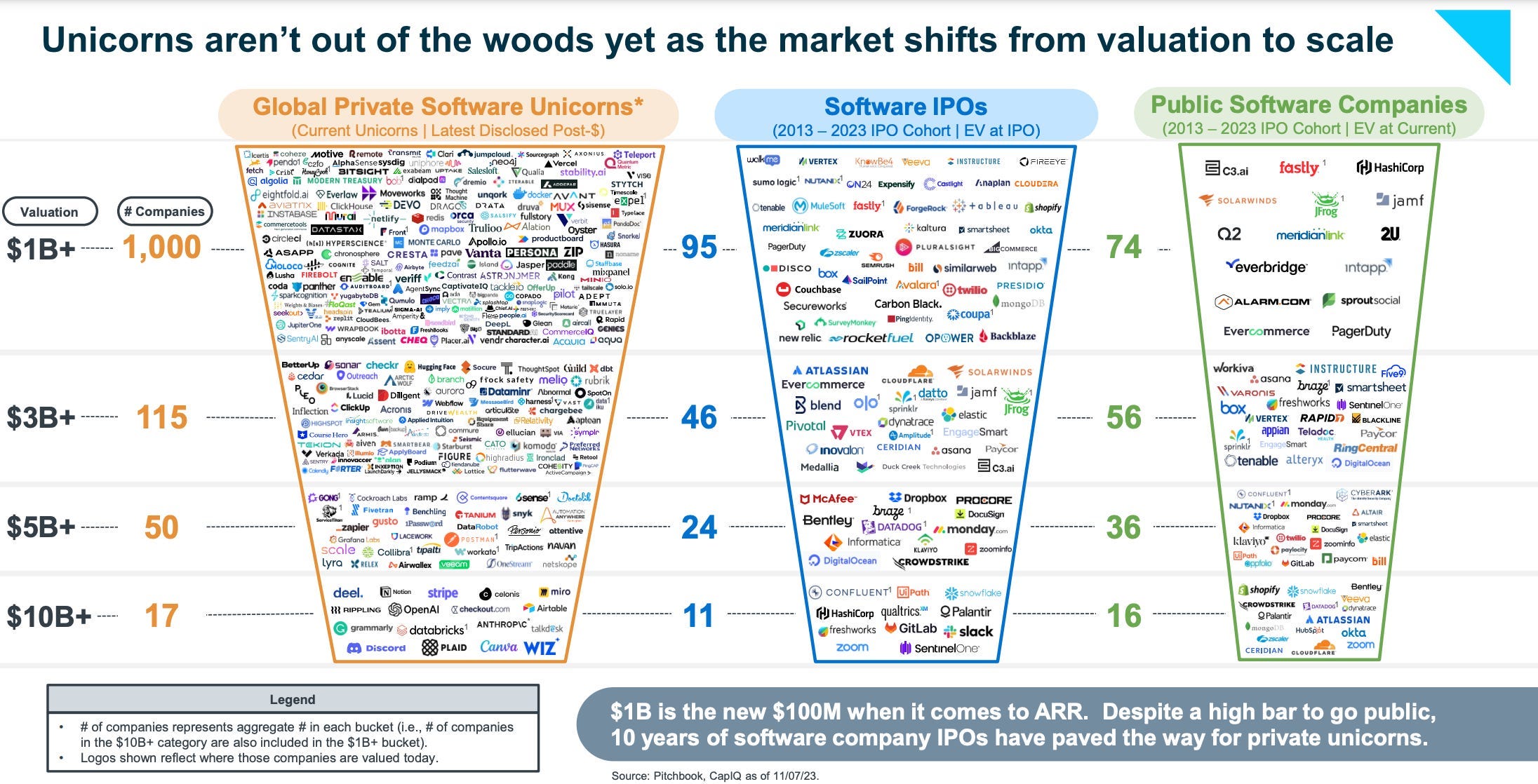

Now, here is a chart from our friends at Battery Ventures.

I would encourage you to spend a few moments looking at this chart. Per Battery folks, there are only 74 publicly listed software companies valued at $1bn or above.

To get to our 3x DPI, we will need at least 10 of these in our portfolio. The gods of mathematics do not smile beatifically on the probability of our being able to do that.

Hunter Walk’s framework of “who gets to eat” in VC is especially relevant here. TLDR: Seed/Series A funds with high ownership get to eat at the $1B exit level, whereas you’d need $10B exits for everyone on the cap table to eat. Relevant posts here and here.

My conclusion from this entire exercise is this: shit’s hard, yo!

B. Where do we go from here?

I think 3 possible trends playing out in the Near/Medium term:

VC market will contract: We are already seeing shops shutting and exiting markets. Stupid money would either be scammed away or shut shop owing to poor returns.

The Rise of the Solo GP: It is hard to raise money as a solo GP. conventional wisdom is that you need another brain to help you look through your own blind spots. However, now that the Macro is going to force the LPs to focus on a smaller number of higher performance GPs - solo GP funds can likely be extremely effective. They don’t need as much fee to sustain operations. They can use AI for sourcing, diligence, and back-office and match the capabilities of much larger rivals. Most importantly, a solo GP can move much faster on deals vs. needing to reach consensus within a given partnership8.

Calm Funds: I also see a return to more sensible investing in a new kind of company - cash flow generating, insanely profitable, fast growing (but not venture growth) which doesn’t need to generate as much money in exit value and can actually pay out distributions. I am very excited by what AI will do in this area. A great example is niche software9.

C. Closing Thoughts

There will be always be fee chasing behemoths whose LPs need strategies that deploy large amounts of capital or the cred - and that is perfectly fine.

What is much more encouraging for me is the potential for disciplined, right sized funds and solo GPs who are capacity constrained in how many investments they can make.

Very, very interesting times lie ahead.

Housekeeping:

As always, I look forward to hearing from you. If you liked this post, pls feel free to share this or subscribe to this newsletter using the links below. I try to write a 1000-2000 word essay once every 4 weeks or so.

beyond brand pedigree, number of ex McKinsey consultants on rolls, platform support, not taking board seats, etc.

read spending 18 hours in front of spreadsheets and second guessing yourself 15 times a day.

DPI is distributions to paid in capital, which is the dollars actually paid back to limited partners. TVPI is total value to paid in capital, which includes DPI, as well as gains that have yet to be realized.

Assuming no recycling and no roll-off of fees.

Per Crunchbase, it is a bit higher but I wanted to keep round numbers.

$250mn difference is the GPs carry.

A $500mn fund I worked at was paralyzed because of two partners being at each others heads. If one said day, other said night, irrespective of what the clock might say.

Niche software is complex to build, and has limited market size, so has historically been uneconomical to fund large teams addressing comparatively smaller markets. Assuming the leverage that AI gives to software development teams continues to increase, we’ll see these more niche ideas becoming economical, and the calm funds which fund them also become viable.