SPACing away to glory.

Chu***a banaya bada maza aaya....

Hello.

How have you been? World has had some interesting moves since my last post. As we speak, Iran is going through another revolution, and Russia is mobilizing reserves. Both are probably regime-ending developments.

However, another very loud, in your face, almost Trumpish-in-its-garishness regime is dying (maybe already dead). Let’s lay a wreath on it today.

Dying SPACs

In December 21, I wrote a list of predictions for the coming year. #5 on the list was:

“SPAC Merged companies will increasingly be taken private by the Sponsors. Saying that the performance has been crappy is a massive understatement. It is also very likely that money will be returned to investors - there will likely be no place to deploy it. Here’s looking at you Chamath.”

I have since been waiting patiently. Then, 6 days ago, this happened.

“Chamath Palihapitiya will wind down and return cash from the two special-purpose acquisition companies to shareholders after failing to find companies to take public. Giving up is an admission by the brash venture capitalist dubbed the “SPAC king” that the market that helped make him a mainstay on business television has effectively shut down.”

Bloomberg was more snarky:

1. Some Observations:

Before we begin, some general observations.

Whenever something with ZERO revenues is worth a Billion Dollars, see if you can short it1. Perpetual / power perpetual options anyone?

Whenever someone is touted as the next Buffett, an implosion is not very far away.

Whenever a new innovation / startup / platform tries to democratize or uberize or bring-to-the-masses something, those newly democratized, uberized, unwashed masses are inevitably going to be left holding a bag of something. Usually a bag of crap.

2. Chamath Who?

I first heard of Chamath towards the end of 2020 when I ran into this tweet about Metromile2:

I read it, shook my head, moved on. Then, sometime in January, I found a Reddit thread about SoFi. Folks had gone insane about Chamath’s announcement of taking SoFi public via a SPAC. One punter wrote that it would be a

“stock that you buy with hopes of transforming you into a millionaire”

He (Chamath) unveiled the $8.7 billion deal to the public on 7th Jan, 2022 on Twitter (naturally). Nearly 65 mn shares of Chamath’s Social Capital Hedosophia Holdings Corp. V (ticker: IPOE) changed hands that day. At the end of that day, IPOE was up 58% at $19.14, even though the deal wasn’t final and the SPAC had NO ASSETS. It almost seemed like Chamath had entered the rarified layer of stratosphere usually reserved for the likes of Elon. They tweet, millions buy.

WSJ called him the SPAC-man. In Feb 2021, he was dubbed the King of SPACs by Bloomberg.

Of course, Chamath didn’t back down or display any humility. He leaned in. if you have the time, watch this video. Chamath says:

"Nobody’s going to listen to Buffett. But there has to be other folks that take that mantle, take the baton, and do it as well to this younger generation in the language they understand.”

Yup. Chamath has done it to the younger generation alright. Done ’em well…

3. But, Why SPACs?

SPACs or Blank Cheque companies are basically a shortcut. See, normally, an unlisted company seeking to go public needs to do a ton of work (easily 12 to 18 months if not more) to get listed. Then there is the paralyzing uncertainty about the reception by investors and if there will be any buyers. SPACs on the other hand are listed companies who have already raised funds and are looking for businesses to buy. They have already gone through the effort of getting listed so private companies can reverse-merge with these SPACs and get listed thus. The merged entity then trades under the name of the private company.

Now, of course, this is simplified a lot but mostly, SPACs are a good way to get liquidity, quickly. ALL private investors worry about exits so SPACs are very attractive for them as well - instant liquidity on tap without any of the hard work of the IPO.

Now, this is normally a win-win-win situation. SPAC sponsors get free shares for successful deals. For the private co, this is a lot less riskier and expensive than going IPO and for the general public, they get a shot at insider prices for great companies.

So, you may now want to ask me. WTF happened?

You see, SPACs have been around for a very long time. Only in 2020-21, they stopped paying attention to numbers and became storytellers.

4. A Good Story can be worth billions

I graduated from business school in 2008. Call it a vintage effect, call it shared misery but most people I know of my “vintage” (i.e. people who entered the world of high-finance from 2006-2009) are mostly numbers people. I worship on the altars of cash flow, unit economics and revenues. And those usually give me a sense of what valuations to offer.

Most VCs would agree that high level unit economics and dynamics of a business are usually understood in about 30 seconds. Understanding the defensibility and risks/uncertainties embedded in those unit economics and dynamics typically takes all the work involved in making an investment.

But, numbers don’t make for hype and stories. Far too often, Fundamentals are ignored for stories.

Let's look at last two years in the markets. Can anyone honestly say that the last two years were about fundamentals? They weren’t. We had a bull market, increasingly easy money. People were more interested in what an asset “could be”, and were therefore willing to pay insane premiums for which priced in perfect market conditions, perfect economic environment, perfect execution and perfect decision making. The market (read retail investors) paid premiums for stories.

Needless to say, now that the easy money is drying up, suddenly the focus has been yanked back to fundamentals. The same pundits who were valuing companies on adjusted community EBITDA are now talking about Cash Flows, RoEs and RoCEs.

Most SPACs were about stories. Then the easy money dried up.

5. How? Isn’t going with a SPAC a slightly easier version of an IPO?

NOPE.

Here’s why: See any IPO prospectus. These will have a ton of details about the company. An IPO prospectus contains extremely detailed financials, all errors of omission and commission, detailed views on market, business, competition and so on. Basically - an IPO prospectus is not very different from a highly unpleasant cavity search3. Any red flags are immediately visible and what's better, have to be disclosed. By Law.

One thing you can’t include in IPO Docs - Projections. Absolute No No.

In contrast, here is a look at a slide in SoFi’s presentation about its merger with a Chamath SPAC:

SPACs can make projections. IPOs can’t. It’s a huge difference. And good numbers + compelling story is a combination that is catnip to Humans.

Think about the environment in which these projections were made - zero interest rates; questionable GIFs trading at millions, tech stocks trading at 50-100x revenues, everyone was working from home and day-trading to scratch the gambling itch in their version of atlantic-city-at-home.

The prevailing sentiment was - “screw fundamentals like cash flow and revenues. Fundamentals are for p*****s.” Well, guess who’s laughing now4.

Of course, things have changed since. Interest rates are not zero anymore, FAANGy stocks have cratered, Everyone (almost) is back to work. Stories aren’t valuable in this environment. And if the story isn’t cutting it - one better have strong fundamentals.

SPACs were supposed to democratize investing. Instead, they leave behind a lot of broken dreams of those who got convinced that these companies would one day make a ton of money. The only people who got rich were the SPAC sponsors.

6. Closing

Irrespective of what one might think of Chamath - credit where credit is due - the guy is a twitter whisperer. He played the platform like only Elon has been able to, he played the inequality and climate change cards like a boss and like Elon, his tweets could move stocks to 2-3x immediately.

Sticking with Sofi - Here is the original tweet about Sofi merger:

I don’t know about you - but I don’t see any analysis or even an investment thesis in here. I do see a pump-and-dump. A legal one at that.

So, in the opinion of this observer, here is what Chamath’s playbook seems like:

Invest in a company

Spin a convincing story.

HYPE HYPE HYPE.

Get your social media followers to buy.

Sell your holdings once lock-in ends.

Rinse, Repeat.

It’s not a bad strategy when it nets you $750mn from investments that are down almost 70%. From WSJ

“The founder and CEO of Social Capital Holdings Inc. said in an interview that the company has made about $750 million in SPACs, roughly doubling its money. The gains come from the six deals it completed such as SoFi. SPAC creators are protected from big losses through lucrative incentives. Social Capital creates its SPACs by partnering with other investment firms.”

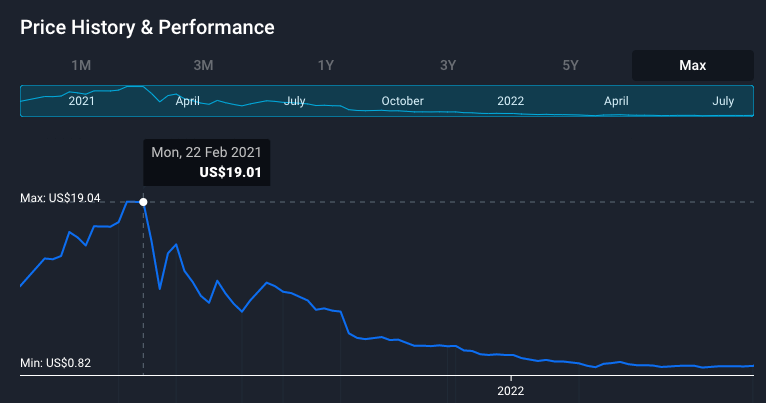

They say a picture is worth a thousand words. Here is the carnage in all it’s technicolor glory:

Reflecting on whatever Chamath has done - it may not be illegal - after all, no one put a gun to another’s head and forced them to invest. It certainly is highly unethical. If you ever wanted to see the greater fool theory exploited to make money - look at Chamath.

Housekeeping

As always, I look forward to hearing from you. If you liked this post, pls feel free to share this or subscribe to this newsletter using the links below. I try to write a 1000-2000 word essay once every two/three weeks.

And if not, run away from it at breakneck speed.

Metromile crashed by 90% before it was acquired by Lemonade in July 2022. Here is Metromile performance before it was bought out.

I am told…..

One of the earliest subscribers to this blog is a day trader. She has shorted every Chamath company every day for last 18 months. I asked her why. Her reasoning was that the valuations bake in perfection. It will not happen. They have made nearly 12x money. Most likely, this is a most impressive, top decile return in the history of money markets. But then she likes to short everything so maybe it’s a lucky break. Who knows…