Hello.

It’s been a couple of months. I was travelling. There was nothing interesting to write about. In the meanwhile, this newsletter quietly celebrated its 2nd birthday. I can only thank you for reading.

In other news, a fight is brewing up in my condo. Some owners do not want people bringing outside trainers. People who need outside trainers are understandably upset. Owners are old people who are lucky if they can go for a walk. Gym users are younger tenants. Much whataboutery abounds. Some people wrote messages in favour of banning external trainers in the gym register. Someone else asked them to fuck off in writing. People got offended that their blatant attempts to use a register as a campaigning tool were met with written hopes that they get cancerous butts. Much entertainment. There is a grand showdown scheduled for October 15. Yours truly will be there to lend gravity to the pro-external-trainers faction.

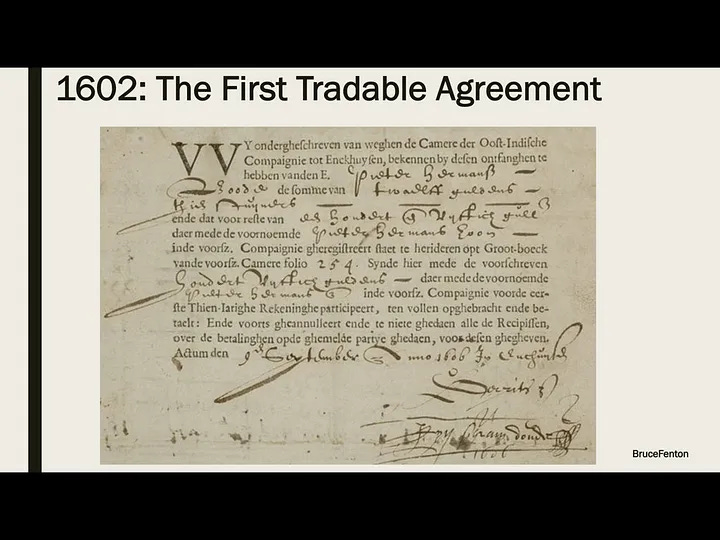

On my last trip to Amsterdam, I met a friend at the Amsterdam stock exchange. It is one of the bastions of the modern financial system - it is one of the “oldest”, “modern” securities markets in the world. It was established in 1602, shortly after the formation of the Dutch East India Company (Verenigde Oostindische Compagnie or VOC). VOC shares traded in the secondary market. A chance stroll through one of the bookshops in the area led me to this gem:

Now, I have read Mr. Mackay before but not Joseph De La Vega’s book - it is from 1688 - about 350 years old. I had to buy it. Turns out, my relative lack of knowledge about this book did not mean that others had missed it. HBS published an english translation in 1957 and in an FT article from 1995, the Editor picked Confusion De Confusiones as one of the ten best books about investing ever written. Now, before we go further, a brief history lesson.

World’s first IPO

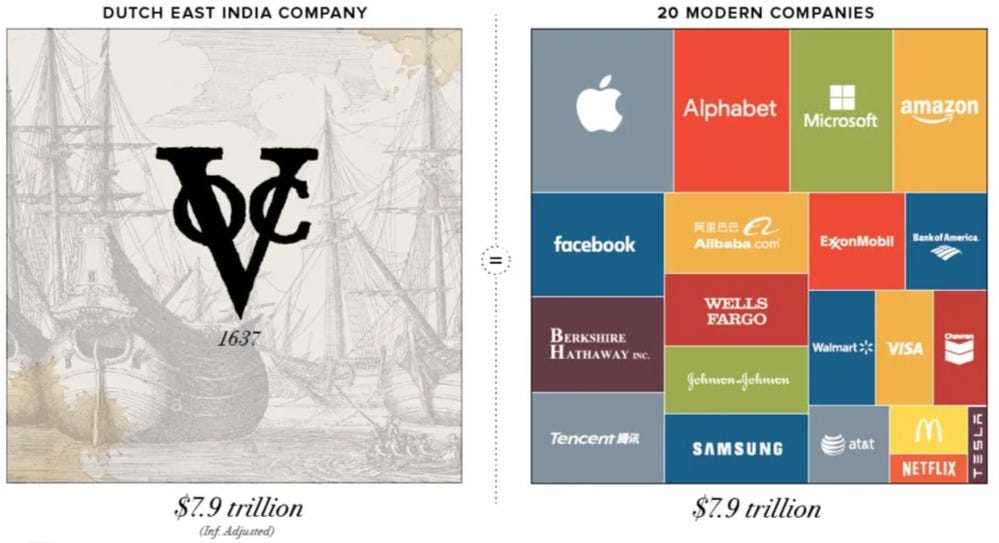

VOC launched its IPO in August 1602. It was the first IPO in history. It was public - “all the residents of these lands, may buy shares in this Company” proclaimed an article in the company’s charter. Now, sure, companies had existed before but this was the first time in history that every Dutch citizen could invest in a company.

The initial time frame for the company was 21 years. In a time when the average life expectancy was a about 40 years - this was too long. So, the directors of the company, in their wisdom included a provision to liquidate the VOC after 10 years. And even this was deemed to be excessive. So, the charter included a historic provision:

“Conveyance or transfer (of shares) may be done through the bookkeeper of this chamber”

Investors did not need to wait till 1612 to get their money back - they could simply sell their shares. The Dutch kept innovating - coming up with such bewildering concepts like forward contracts, short selling, derivatives and insurance.

At this point, you may be asking - exactly how big was VOC and why is this important - here is the answer.

Yup. Messers Buffett, Pichai, Nadella, Zuckerberg, Bezos and Cook could suck it.

Of Unfair Trade Practices

Short selling today is more or less taken for granted. History is a bit more colourful.

Isaac Le Maire was a Dutch businessman, an investor and a constant thorn in VOC’s side. Now, the story is a bit more like someone scorned but interesting nonetheless.

In 1602 (IPO year), Le Maire applied for VOC shares worth 85,000 guilders. This made him the largest VOC shareholder and he was appointed as the High Governor of the company. Due to some financial improprieties, he was forced to leave the company in 1605 and was soon invited by Henry IV of France to set up the French East India company.

Le Maire was not one to forgive or forget. So, in 1609 he and eight others founded a secret company with the purpose to trade in VOC shares. This so-called "Grote Compagnie" sold naked short1 shares of the VOC. Le Maire hoped that the competition by the French East India Company would ensure that the share price of the VOC dropped like a stone.

However, the French company was shelved. A little miffed at its fortunes, the Grote Compagnie resorted to blatant rumor mongering to depress the prices anyway. Now, in an age where information was not available the way it is today - the strategy worked. VOC shares tanked.

At the time, this was some incredibly sophisticated machination.

I quote from Lodewijk Petram’s The Worlds First Stock Exchange:

“Le Maire and his syndicate used forward contracts for their bear raid. Selling borrowed shares would also have been an option but was more difficult to organize. Trading forwards was comparatively easy and all it took to strike a forward deal, was a written contract and it was not customary to ask for collateral.

These forward deals were agreements that established that the parties would trade a VOC share at a particular time in the future at a price set at the moment that the transaction was entered into. They are comparable to modern-day futures contracts, but where futures are standardized contracts, each forward was negotiated individually. Forward trading was convenient to share dealers as no share was transferred, and there was no need to pay anything at the time the contract was signed.

None of this happened until the contract’s end date. And even then, it was not necessary to transfer the share as traders could opt for a cash settlement, which would offset the price in the contract against the spot price at that moment.”

The VOC was predictably - unhappy. Petitions to the highest authorities in the land ensued. VOC blamed “vile practices” that were “very disadvantageous to the investors and particularly the many widows and orphans.” Le Maire resisted and claimed that the price drop was the result of the bad course of actions of the VOC (and this claim was not without some truth).

Well, as had happened and has continued to happen - extremely rich people using widows and orphans as human shields won out. In Feb 1610, sale of shares not in possession was banned. And so, shorting as we know it now came into being - borrow shares and sell them.

In the aftermath - Le Maire lost his shirt and retired completely from Amsterdam. Such is the power of 17th century Dutch widows and orphans.

There were further developments related to options trading, straddles, and leverage. By 1650s, there were enough traders with sufficient experience to use these complicated instruments.

Can we get back to the book please?

Well, Let me start with a quote from Vega’s Book. He writes:

“If one were to lead a stranger through the streets of Amsterdam and ask him where was, he would answer “among speculators,” for there is no corner where one does not talk shares.”

I mean, Amsterdam’s canals, a small cafe, maybe some potent herbs to smoke, a cup of coffee, a light breeze. It’s only natural to talk shares and derivatives.

In many ways, the book is a precursor to the academic study of modern behavioural finance. He not only describes kneejerk, even excessive trading but also markets overreacting and what I assume is the first description of the disposition effect.

The book is a lot less about more mechanics of trading but about the people making the trading decisions. Here’s is another telling quote:

“When the speculators talk, they talk shares; when they run an errand, the shares make them do so; when they stand still, the shares act like a rein; when they look at something it is shares that they see; when they think hard, the shares provide the content of their thoughts; if they eat, the shares are their food; if they meditate or study, they think of the shares; in their fever fantasies, they are occupied with shares; and even on the death bed, their last worries are the shares”

Eventually, the book outlines 4 principles of speculation, with highly evocative imagery involving eels, carbuncles, stones, morning dew and chimeras:

“The first principle [in speculation]: Never give anyone the advice to buy or sell shares, because, where perspicacity is weakened, the most benevolent piece of advice can turn out badly.

The second principle: Take every gain without showing remorse about missed profits, because an eel may escape sooner than you think. It is wise to enjoy that which is possible without hoping for the continuance of a favorable conjuncture and the persistence of good luck.

The third principle: Profits on the exchange are the treasures of goblins. At one time they may be carbuncle stones, then coals, then diamonds, then flint-stones, then morning dew, then tears.

The fourth principle: Whoever wishes to win in this game must have patience and money, since the values are so little constant and the rumors so little founded on truth. He who knows how to endure blows without being terrified by the misfortune resembles the lion who answers the thunder with a roar, and is unlike the hind who, stunned by the thunder, tries to flee. It is certain that he who does not give up hope will win, and will secure money adequate for the operations that he envisaged at the start. Owing to the vicissitudes, many people make themselves ridiculous because some speculators are guided by dreams, others by prophecies, these by illusions, those by moods, and innumerable men by chimeras.”

So, are you a lion roaring at thunder or are you an escapist eel?

Contagions and Crashes

I quote Mr. Vega again:

“In science and technology, progress is cumulative, but in finance and investing, progress is cyclical”

You know, that is a remarkably prescient observation from someone writing in 1688. de la Vega may have been the first to articulate and record the irrational behaviour but over the past couple of centuries, various others have identified and warned about this. In the 1840s, Charles Mackay used his observations and came up with the basics of behavioral finance in his book, Extraordinary Popular Delusions and the Madness of Crowds (second of the two book combo I purchased). He chronicled various crashes. He writes:

“We find that whole communities suddenly fix their minds upon one object, and go mad in its pursuit; that millions of people become simultaneously impressed with one delusion, and run after it…

Sober nations have all at once become desperate gamblers, and risked almost their existence upon the turn of a piece of paper…

Men, it has been well said, think in herds…go mad in herds, while they only recover their senses slowly, and one by one.”

I don’t know about you but it does remind me of the last 6 years. Wework/Theranos, anyone?

Contagion and crashes are often a good starting point for understanding psychological behavior in the markets. One of the most remarkable characteristic of speculative manias is their similarity, even if hundreds of years apart. Each mania had sound beginnings and was built on a simple but intriguing concept. Soon after, common sense often found itself defenestrated by the almost complete abandonment of basics and application of intellect. People believed believe each bubble offered offers opportunities far more enticing than they had have ever seen before. In each mania excessively risky actions were are justified as prudent. Chamathing2 is a thing.

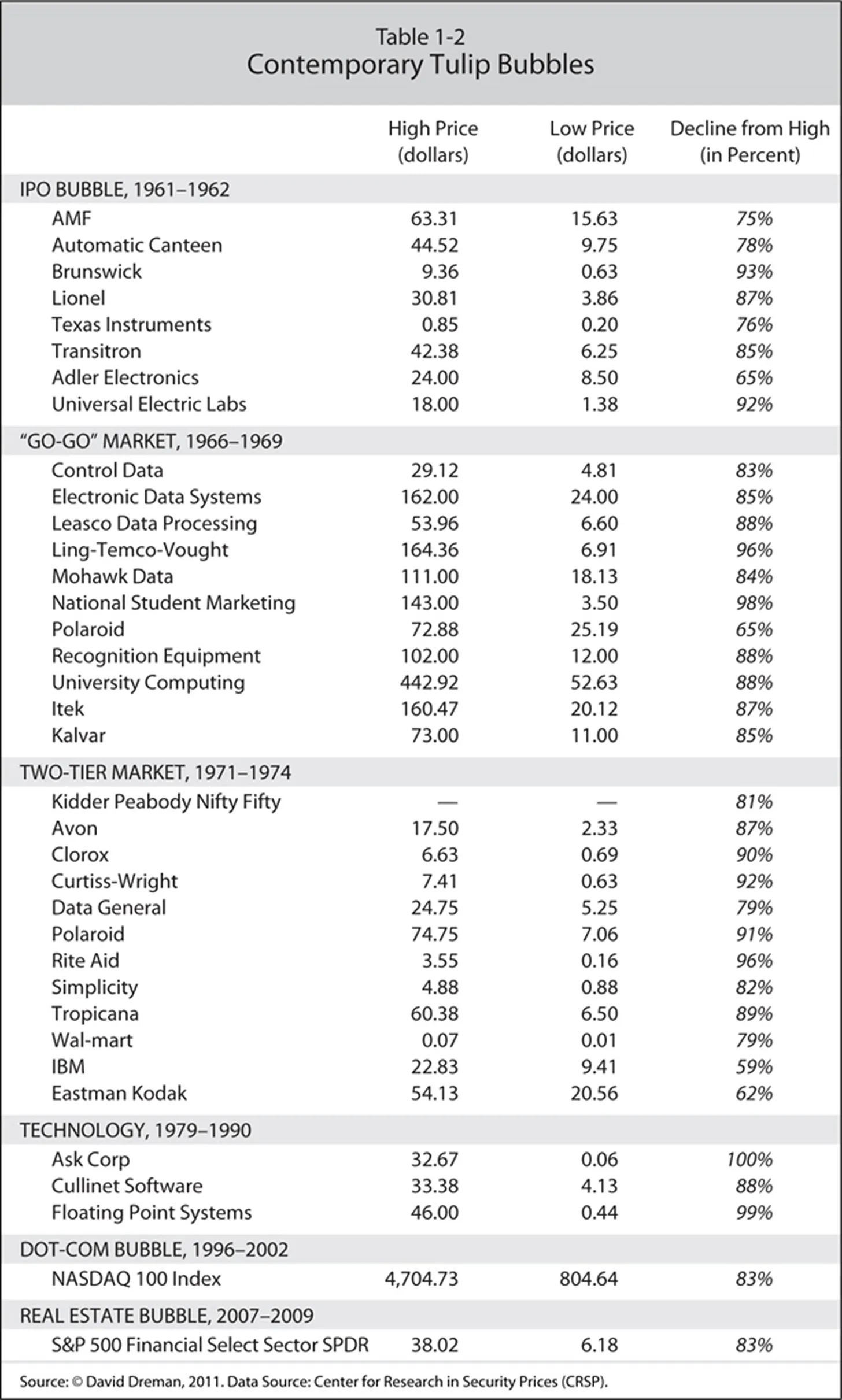

David Dreman writes in Contrarian Investment Strategies (Classic Edition):

“In a bubble any torrid concept will work. Investors in each mania have believed and followed pied pipers. Though bubbles provide almost endless jubilation on the way up, the way down is like entering Dante’s eighth circle of Hell. In every bubble, once the crowd begins to realize how wildly overpriced the stocks it rushed into are, there is a scramble to escape. A horrific panic ensues as the image changes from euphoria to doom. Rumours always play a major role, at first of fortunes being made and of good things to come and then later of prophecies of doom. Finally, prices fall back to where they started off or lower. The curtain has dropped, and the riveting drama is over. Perhaps the most curious similarity of all is the sharp percentage drop from each high-water mark, on the order of 80 to 90 percent or more.”

The he goes on to present two tables. I’ll leave you, dear reader to take away from these what you may like:

Concluding:

Modern behavioural finance is based on 3 key concepts (as far as I can see it). These are:

Nobel prizes have been awarded to people who came up with these. Which only goes to show that likely, no common sense is needed to win a nobel in Economics. If anything, a decent amount of common sense is in fact a detriment.

Today’s investors are remarkably well-educated. They have access to unholy amounts of information, state of the art tech and finest experts/research money can buy. Yet, the gap between bubbles and crashes only seems to be getting smaller.

Dead and walking-dead economists have probably done more damage to investors wealth than anything else combined in the past century.

Interesting Reads:

Tenochtitlan, brought to life. Brilliant, brilliant visualizations.

Google and Traffic Acquisition costs - I am eagerly awaiting the court filings. Also, bonus tip - if you want to bypass paywalls, use archive.ph.

Ben Evans on AGI and IP - very well argued.

DMA rules go in force in Europe. On the whole, positive, irrespective of all the gnashing of teeth and rending of clothes on display by Apple, Google and Microsoft.

Housekeeping

As always, I look forward to hearing from you. If you liked this post, pls feel free to share this or subscribe to this newsletter using the links below. While I have been tardy of late, I try to write a 1000-2000 word essay once every 4 weeks or so.

Naked Short - selling shares without actually owning them

Chamathing - (verb) The act of using SPACS to buy BS companies and selling them to retail investors by hyping them up on twitter - they all lose money even as the chamather makes money as being the SPAC sponsor.