Google and a tale of two telcos.

Airtel and Jio - both? Hedging Strategy or Strategic Hedge?

About a week or so ago, Google announced a billion dollar investment in Airtel. ~70% will go in as cash, rest as services / contributions.

Great news for Airtel, except that in 2020, Google had already invested in Jio. A small sum of only $4.5bn. Now, at that time, I could see the whole Jio / Google play. Jio’s vertical play was in so many ways, a once in a lifetime opportunity and something Google could make very good use of.

So, why put a significant bit of change in creating the telecom equivalent of the bollywood love triangle?

Allow me to take a very meandering take on this. Here we go.

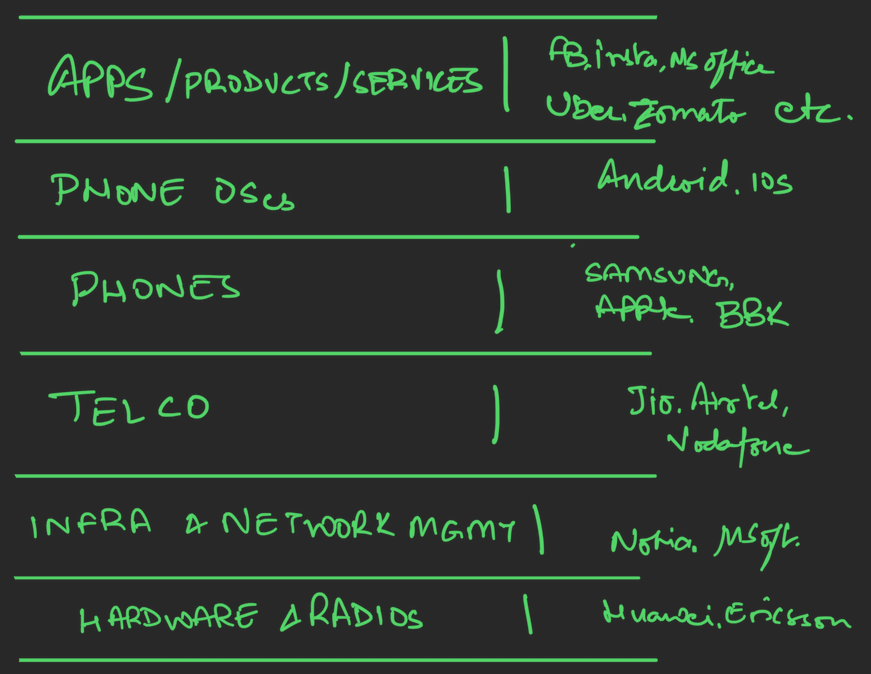

1. The Telecom Stack

Before we begin in earnest, a bit of context.

When the mobile telecom revolution began, bandwidth was at a premium, adoption was low. This led to voice and SMS being the key modes of the pipe. And this pipe was very thin. As the technology has evolved, the net effect has been a widening of the pipe. So much so that when you are using VoLTE, you are effectively making a call using the internet.

As the tech evolves, (see above) the fatness of this pipe is changing - which has enabled richer applications to be built on top. However, it has also had the effect of reducing the modern telco to a data pipe and little more. I have not made an international call outside of whatsapp or zoom in more than 5 years. Why should we pay extra when we can simply make a call using wifi or the internet? At one point in time, my phone bill used to be almost INR 5000 / month. Now it is INR 300/month.

As such, the telco is increasingly becoming the equivalent of the network layer in the TCP/IP stack. Here is what the telecom stack looks like:

The value is increasingly captured by the people at the top of this stack. The ones at the bottom face inevitable commoditization. However, the ends allow for scale due to specialization (low end) and value capture(high end). The Telcos are in a pretty unenviable place in the middle. They can be hit from both sides and effectively are unable to control their destiny beyond a point. In effect, they are price and volume takers.

This change has taken a long time coming, and is only obvious in retrospect. The erosion of traditional voice (international and long distance calls) revenue has been offset only by the exploding data usage. Otherwise all mobile network operators would have died. Come to think of it, they have. The recent travails and effective nationalization of Vodafone India is a case in point. In its heyday, the Indian Telecom Market had more than 15 operators. Now there are 4. Two are effectively owned by the indian government.

2. Survival in a Squeeze

So, if you are a telco today, and you are reduced to a pipe, what are you to do?

The entire Media and Telecom sector is really reorganizing itself on 4 axes - Advertisements, Payments, Social Media and Cloud infra/datacenters. Barring the last one, none of the remaining 3 axes can easily be tackled by a Telco. And that is before expending a few tens of billion USD on each of these. There are cheaper, faster, better alternatives and you can only throw in so many sweeteners by the way of customer acquisition sops.

As a Telco, you may have subscribers, but they aren’t going to use your half baked solutions over the gold standards for each use case. There is a reason by those of you who have subscribed to Apple music use it over Wynk music. The Telcos don’t really have any engagement with the subscribers beyond being internet providers.

The best (and only) way left to control your destiny then? To vertically integrate and control the whole stack. Even if someone came up with the money, the talent and specialization needed is in such short supply that doing so is pretty much a modern Manhattan Project. So much so that most observers thought it would not happen. But then, it began at least…

3. Love in the times of Covid

2020 rolled around. Right as planet earth was poking a fat stubby finger (Covid 19) in the collective right eye of humanity, this happened.

Jio Platforms, a subsidiary of Reliance Industries (India’s most valued firm) has raised about $20.2 billion in the past four months from 13 investors by selling about 33% stake in the firm. (For some context, the entire Indian startup ecosystem raised $14.5 billion last year.)

Google’s new investment gives Jio Platforms an equity valuation of $58 billion — the same valuation implied by Facebook. Other investors, including General Atlantic, Silver Lake, Qualcomm, Intel and Vista, have paid a 12.5% premium for their stake in Jio Platforms.

Established punditry was stunned, left speechless by this crazy event. The names of the investors are very important here. Qualcomm is the leading maker of network hardware, mobile modems / chipsets and radios. Google straddles infra and services. Facebook represents Whatsapp, Instagram and Facebook. Intel chips can be found in the innards of most electronic boxes in our houses.

Jio sold a third of itself to these guys so that it can control the entire stack. Right from its own efforts at building 5G radios to its own apps for meetings, to its own e-commerce platforms.

Here are a couple of screen-grabs from Reliance’s own presentation from that point to outline the extent of the integration.

and

If I look at it as an investor, it’s a sensible moonshot strategy. The thought process is sound and while there is a literal ton of execution risk, it is not something that cannot be addressed by low-hanging solutions (i.e. throwing more money at it).

And yes, there are a whole lot of tailwinds to why this happened but the rulebook was rewritten.

Audacious - Yes.

Risky - immensely.

Inevitable - maybe Yes.

4. Airtel’s Response

Now, when these headlines were splashed across the newspapers, imagine the heartburn it must have caused at the Airtel HQ. Airtel is a company that unlike Jio1, has shelled out unholy amounts of money for spectrum. It has built a very large (and profitable) business. It was hit by a competitor who provided free services for more than a year while the regulator did not immediately put a stop to Jio’s bending of the rules. To add insult to financial injury, all MNOs were forced to provide interconnect points to Jio by the regulator.

Then these headlines hit. I am sure a stream of expletives flowed somewhere. Worst of all, Jio suddenly had a better multiple (~12x EBITDA) compared to the rest of the telecom industry (7-9x EBITDA).

Now, one of the advantages of being Airtel is that it has a lot of stickiness. It has a sizeable base of postpaid users and consistently had higher ARPU than Jio. Jio may have more users but the average Airtel user is more valuable than the average Jio user.

Now, what took Airtel by surprise was the whole ecosystem approach that Jio was touting. It wasn’t that the company didn’t try, but the pieces never came together in a sensible whole. Suddenly, Jio had roped in the global leaders and was effectively saying - “I have allies. I will crush you.”

As an example, Airtel has been in the payments business for more than a decade now. While PayTM and Mobikwik’s businesses shot forward, the Airtel bank as of today is a could-have-been. Think about it, it’s a cash-burn business in a thin margin parent. Of course it wasn’t front and center and it seems was treated like a sideshow. However, it would be wrong to say that there are no meaningful businesses within Airtel. Airtel runs Airtel Ads, the Xstream content platform, a music streaming platform called Wynk. There is a super-appish platform called Airtel Thanks. However, most of these are serving as add-ons to the core telecom business as incentives to build stickiness. I remember reading somewhere that airtel digital had MAUs of ~200mn. Its revenues were estimated at <$15mn for FY21.

So, after about a year, Airtel took a leaf from Jio’s playbook and spun its digital businesses out into a seperate company before raising capital for it. Comprehensive spring cleaning began - Investors were bought out, businesses were consolidated, optionalities were bought.

In these early days 2021, Airtel was telling everyone who listened that they will build their church on the triple rocks of advertising, payments and e-commerce. So, same wine as Jio, in a different bottle.

5. JioPhone 2 - Watershed or Waterloo?

While we are discussing Jio and Airtel, let’s also spend a moment talking about Vodafone-Idea. Created from the merger of Vodafone and Idea in 2018, Vodafone Idea just emerged from a near-brush with death after unreasonable spectrum dues were assessed and it asked the government to run the business. In some ways, the Covid situation and the resulting chip shortages saved Vodafone Idea. Had the Jiophone 2 launched on time, Vodafone Idea would have been dead long, long ago.

India is still very much a 2G country. When Jio started, it faced a massive challenge - it was a 4G only network (because it never paid for 2G/3G spectrum) and there weren’t any affordable 4G phones in the market. So here’s what it did - it launched a cheap phone called the Jiophone. For a refundable deposit of INR 1500 and a qualifying plan, you could have a 4G phone. It sold like hot cakes. or, to be more precise - Jio pretty much gave them away. By various estimates, Jiophone alone got jio 80-100mn subscribers.

Jio was aiming to get a successor to its incredibly successful Jiophone - the Jiophone 2. Unlike KaiOS based Jiophone 1, Jiophone 2 was supposed to be a low-cost 4G device running a version of Android. Thankfully for both Vodafone-Idea and Airtel, there weren’t enough chips to go around so Jiophone 2 got mired in delays (more later).

Meanwhile, Airtel also promptly announced its own Indian Smartphone plans. And it’s not like it hasn’t done it before. MTN (Airtel subsidiary) has done this exact same play in Africa.

So, we should be getting two cheap phones that will usher the Indian market into a new age of connectedness. Right?

Wrong.

Smartphones are not cheap to make. The monopolies are even more stark in the cellphone business. And more importantly, the retail price point of any phone is unlikely to be below INR 4000 (unlike 2G feature phones that can be built sensibly at ~INR 1000). No amount of volume committed by Jio or Airtel will pull meaningful production capacity to razor thin margin phones where chips are in such massive shortage, especially when one is asking for 3-4 year old specs. if I were TSMC, would I not rather make high value chips for Apple and Samsung (where I get squeezed even though these companies are able to set their own prices) than for a Jio which has to build to a price?

And then, on Jan 31, there was this.

“Bharti Airtel CEO Gopal Vittal on January 30, Sunday, said that the company has no plans to build its own smartphone but it will partner with OEMs to bring smartphone offerings to the market for the consumers.

"Our strategy is to drive smartphone adoption, we are not keen on the subsidy game, but we want to be competitive in the market,” Bharti Airtel CEO Vittal said, according to reports.”

Ok, So Airtel junked the entire smartphone plan and instead announced an investment from Google.

Now, this makes sense from Airtel’s point of view. Why go through what seems to be a mug’s game (of building phones) when they can integrate in a much deeper level at a higher level in the tech stack of the phone itself. But that begs the question - does that do much for Airtel itself?

I think not. Ok, so you have a partner in Google. Now what? How does that translate into better revenues for Airtel?

Answer - Distribution.

Here it is straight from the horse’s mouth:

“Bharti Airtel's Chief Executive Officer Gopal Vittal on January 28 said the partnership will give a boost to the company's devices, networks, and cloud adoption.”

Airtel’s sales organization now has seriously high quality products to sell.

6. Google’s Lens

Now, let’s look at it from Google’s point of view. Why invest in competing Telcos? It is inevitable that these two will keep bruising each other. So why put one stack of capital in direct conflict with another (and smaller) stack?

See, here is the thing - India has more than a billion mobile users already. and over the next 4-5 years, more than 500mn smartphones will come online. Of this, ~250mn will be people upgrading to smartphones.

For Google, capturing these a critical plank. However, given that the Apple platform has a certain - er - audience, this really isn’t much of a thing to spend a billion $s on. Whatever is not IOS will be Android. Either way, the lion’s share of this incremental base will go to Google. So why invest in a competing telco?

In the opinion of this observer, distribution and an implicit hedge.

Google gets the opportunity to get the users coming and going with both telcos and an opportunity to sell its consumer services and SMB solutions. Google One bundled with your Airtel plan - yes please.

If you look at both apple and google’s P&Ls, you will see that the services revenues are a growing and a highly profitable contributor to the topline. Selling these in emerging markets is however, a tougher proposition. Disposable incomes are not enough to allow people to spend 20$/year on cloud storage.

With these partnerships, Google gets access to sales forces and bundling. And this will allow a significant reduction in the friction inherent in selling these services online.

In reality, the market as far as Google is concerned is a duopoly of Jio and Airtel. VI is not known for the best customer service and its future is at best shaky still. By investing in both companies, Google has effectively managed to get access to the entire market it wants to target.

I would not rule out another billion dollars going into VI one of these days though. Google has $200bn of cash on its balance sheet. Another billion into VI for the optionality can be a no-brainer.

How is that for market dominance?

As always, I look forward to hearing from you. If you liked this post, pls feel free to share this or subscribe to this newsletter using the links below. While I have been tardy of late, I try to write a 1000-2000 word essay once a week.

Jio did not get its start as an MNO. It took a wireless broadband internet license and was able to finagle that into a unified mobility license. That is why Jio network is only 4G. It’s supposed to be an internet service provider. Jio should have killed off BSNL, but it can’t because it cannot provide 2G/3G services. I will invite you to research more on this and if you do, you will be well rewarded by some seriously interesting reading. Here is an article. If you want more, send me an email and I will point you towards a few articles.