Food Delivery has peaked

Customer service is the lever everyone seems to be ignoring.

Hello!!

It has been a few interesting weeks.

As some of you know, a significant part of my net worth is invested in private companies. Now, my theory has always been that meme stonks and growth juggernauts are not the way to go for me. I like to deploy my money in boring, cash flow generating companies. If nothing else, the distributions alone would create a nice passive income stream.

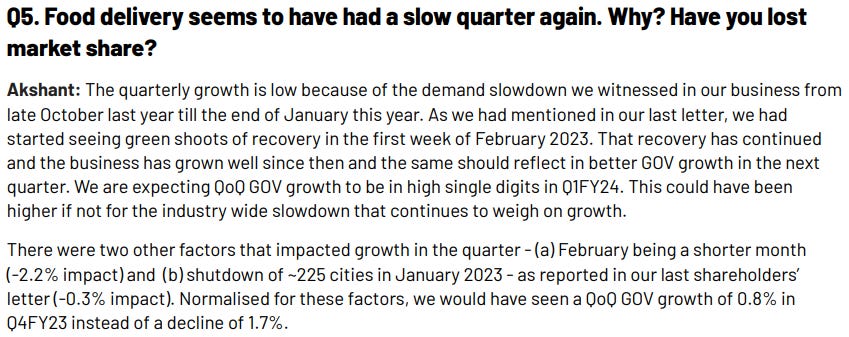

For the last few years, a lot of these investments languished in cash flow purgatory1. The market seemed to be saying that if one was’t growing 100% month on month2, why did one exist at all? My founders were simultaneously disappointed and raring to go. Validation was hard to come by. I was playing philosopher, guide and agony aunt3.

Then the context changed and suddenly this part of the portfolio is being valued and courted like crazy. Let’s just say it is good to have the thesis validated. I am getting out of most of my positions while the going is good.

Zomato letters are a lot of fun to read.

If you have never read Zomato shareholder letters, I would strongly encourage you to do so. You know, not because you actually learn anything but just for shits and giggles. Unsubstantiated self-serving, self-congratulatory statements, EBITDAs being adjusted every which way. Arbitrary effects devised to explain individual performance hits.

Masterclasses in spin.

The full set can be found here and the latest nailbiting thriller here.

Some Misguided Analysis of the Q4FY23 Letter

The letter starts off with the claim that the Q&A format is appreciated. By Whom?

No. This format isn’t appreciated. One would appreciate the management coming on a call and actually answering hard questions instead of feeding us a cherry-picked, spin only narrative. But then, what do I know.

—

Good news follows: I can almost see Deepinder going hazraat, hazraat, hazraat:

Revenue for the quarter is up 70% YoY, losses have nearly halved, food delivery has gone EBITDA positive. Well, adjusted EBITDA positive. Alright, time to celebrate. Let there be champagne etc.

Hold on a minute. Lets go to the tape:

See something here? Food delivery revenues are stagnant and on a downward trend. Hyperpure is starting to slow down (makes sense, picks and shovels have a lag).

—

Then there is Blinkit - the millstone accounting for nearly 560 crores of 780 crores of EBITDA level losses. Ouch.

—

But that is not nearly the worst thing here. GOV and Revenue have hit a wall and are stagnating.

—

But all that is transient you might say. 4 quarters do not make a durable business. I would agree. You know what does make a durable platform business? Customers and fulfillment ability. MAU and delivery partners are also trending down if not stagnant.

For a company with a market cap of INR 560 billion (56,000 crores), this is a really bad place to be in.

—

The only thing that seems to have saved Zomato’s goose is Zomato Gold. You know, the loyalty program they stopped, which sent a whole bunch of their california users to Swiggy and which they have now sheepishly brought back.

If not for gold, Q4 would have looked like flanders fields for Zomato. So I get why the man wants to not answer questions on a call. Because someone like me will call him out on this hare-brained scheme - it’s not as if they didn’t know the contribution of gold customers to their topline. They just thought customers cannot find a better deal for themselves and that the competition is staffed with idiots. Regime changes have been instigated by less.

—

Oh, and BTW, if you thought this question was self-serving and turned into a softball, wait until you see this one:

Let me tell you - this is the first time ever that February’s 28 days have been a factor. Last year, Zomato had a record march quarter. Suddenly seasonality is the big bugbear. I call BS but then, once again, what do I know.

Warm and Fuzzy Feelings FTW

Here is the TLDR of the letter:

The trouble is - this company still burned a 100 crores of cash in the last quarter. Somehow people seem to be ignoring a key factor for all these high-growth, techy, ZIRP stocks: profits and growth are inversely correlated. You cannot have both. Even in the current quarter, they slashed discounts to shore up profitability with near instant hits on the topline.

So, for food delivery, you cannot deliver more profits without significant revenue growth. Hyperpure is not big enough - which leaves Blinkit as the only lever available.

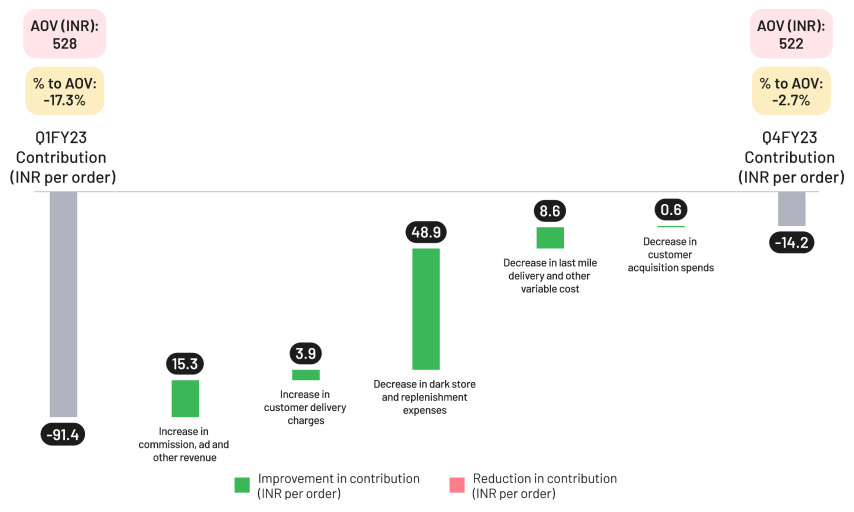

Now, Blinkit seems to be on the right track if we are to believe this bridge:

The problem here is this - hyperlocal delivery can be an extremely profitable business but in limited geographies. The key risk, the key agency problem for Zomato shareholders is that at some point the Man will try to force juice out of Blinkit by forcing scale. Scaling will burn cash. Which will lead us back to square 1.

Mr. Rock, meet Mr. Hard Place.

Nod to Amazon:

Growing Ad revenues. ;)

Takeaways:

In the opinion of this observer, there is an underlying dynamic for all delivery fee based business in India - we desi customers don’t like to pay for Delivery. Don’t blame us. These delivery businesses got us hooked by mainlining uncut discounts straight into us. I mean - come on. It was someone else’s money these companies were spending to create value for themselves. Why not.

However, now that the rock-n-roll party is over, the customer is still jonesing for the discounts. Any brand loyalty these companies imagine can only be found in the trash bin. A 10 rupee differential will move the customer from one platform to another. What will keep a customer - high quality customer service. Ordering food sight unseen is not a problem. Being told to forego the money because zomato is very sorry for the poor experience is.

We have seen this play out before with Flipkart and Amazon. Eventually Amazon won out - because Flipkart’s customer service sucks. Not discounts, not delivery fees. Customer Service. Reliable, customer friendly, resolution focused.

Now, Zomato and Swiggy, both have shitty customer service. Their view of customer service is taking money from customers and trying to claim “we are just a platform” in case of a problem. Any attempt to get any resolution is met with apologies and requests for another chance. They will fight tooth and nail to avoid giving the customer a replacement or a refund. Customers have had enough of this crap.

Whichever one of these companies is able to offer Amazon like Customer service will own the market.

Too bad that it’s not in their DNA.

Which is why this observer submits that food delivery has peaked and the changing context is just not conducive to bonfires of hard cash. Maybe both of these (Z and S) should die so that a new bunch of companies can fix the tilted market.

Asides:

ONDC Elevate Deck. Fascinating read to say the least.

Housekeeping:

As always, I look forward to hearing from you. If you liked this post, pls feel free to share this or subscribe to this newsletter using the links below. While I have been tardy of late, I try to write a 1000-2000 word essay once every 4 weeks or so.

You have Cash flows? Who cares. We are looking for people who can spend our money. BURN BABY BURN!!

Funded by silly money. Oh you are not from an IIT/IIM/MBB network? Sorry, you can’t have our silly money to spend.

None of which I am qualified to do, BTW. All I can do is pour them an old fashioned and top shelf whiskey.

Isnt akshant a subscriber?