Deep Dives #2 - Video Games

who remembers Carmen Sandiego?

As I write this, I will be 37 in a few months. I feel middle aged. I have a paunch and my hair are divorcing me on a daily basis.

I was a bit lucky to get access to a computer as early as 1993. Most of my childhood featured the dulcet tones of dialup modems as the soundtrack. But internet was expensive, so Video Games were the way to spend time. Too much of it. From adventures like Where in the world is Carmen Sandiego, to classics like Mario, Prince of Persia, Road Rash and Need for Speed. Then I got to college, found the twin religions of Age of Empires and CounterStrike and never looked back.

I am an avid PC Gamer. I have not really managed to use consoles but I still, even at this age, find playing video games surprisingly relaxing. Of late I have been enjoying Cities Skylines and Hitman Series.

Research what you love and you won’t work a day in your life… or something like that… right? Anyway, apologies for the hiatus. Researching this one and compressing it to a single read took some time.

OK, let’s dive in.

Industry Map

Now, for the most part, this is an absolutely fascinating value chain. Some layers (like game development and distribution) are fragmented while others (digital distribution) are oligopolies. Publishing is sort of, kind of in the middle - it has about 13 major players. Some like Microsoft and Sony are vertically integrated with their grubby paws everywhere.

Then there are legends like Konami, Sega and Atari.

OK, let’s take a look at 7 key trends driving the industry and influencing its future trajectory.

1. Rise of Digital Distribution

For the longest time, if you wanted to buy a game, you had to buy a CD/DVD of the game. Typically, you went to Amazon, GameStop, Best Buy. However, as payments tech, internet connectivity, infrastructure and tech capabilities (especially DRM) have improved, things have moved forward enough to allow direct digital downloads for games. Per publishers I spoke to, the migration to digital channels for PC games is slowing a bit but consoles are seeing a consistent ~7% shift from physical to digital each year. Overall, physical now accounts for only 20% of PC game sales and ~50% of console sales.

What this means is that the gross margins are expanding. For publishers, the gross margins for digital distribution are ~70-75% - far better than the ~50% GMs in physical distribution. Overall, I would expect 90-95% of all sales to become digital over the next 5-8 years, and corresponding margin expansions for publishers. overall, gross margins should settle at ~80% after factoring in micro transactions (more on that later). See chart on unit economics below.

Now, there is another interesting play happening in the distribution space - which is the platform fees. For almost 18 years, Valve had a monopoly on the distribution of PC Games through Steam. Steam had a nearly 80% market share and a pretty decent DRM platform. So, publishers signed up. Now, Valve got a little greedy and at one point asked for a take rate as high as 30%.

In 2018, Epic had had enough, and they launched the Epic Game store charging only 12%. Steam had to come down to a blended rate of ~20%. I would expect Steam’s take rate to be under even more pressure going forward, especially since publishers are launching their own distribution platforms (assuming these platforms work properly).

EA origins is a good example of bad execution - in 2012/13, EA pulled all their content from Steam. Revenues promptly tanked (Given that Origin wasn’t a very good platform anyway). Net Revenue fell for 7 straight years until EA came back to Steam in 2019 when the revenues promptly increased by 30%.

So, take rate pressures or not, Steam still is the market leader, it enjoys an engaged and large community, and will likely survive regardless.

2. Mobile/Casual Gaming

As mobiles have become more and more capable, and as the price of this capability has lowered - the mobile and casual gaming space has exploded. At one point in time (and for that matter, even today), you needed to spend $1000-1500 on a decent gaming rig or console to play anything. Today, you can play the best titles on a $300 phone. Over the last 10 years or so, PC and Console gaming has grown at a CAGR of <10% - Mobile gaming has grown at a CAGR of almost 30%. And it is quite unlikely this will slow down anytime soon. Per Newzoo, there are ~730mn Console Gamers, 1.3bn PC gamers and a crazy ~2.8bn mobile gamers worldwide.

However, this doesn’t come without its own unique problems. PC and console gaming usually imply focused time blocks. Attention is not usually divided. Mobile is by definition, casual. So - the immersion for the gamer is shallower, and hence, it is harder to monetize than PC or mobile games.

As an example, you can read the ATVI investor decks here. You’ll see that over the last few years, MAUs for King (the designated mobile brand) had been ~5-8 times that of Activision (Call of Duty) and Blizzard (World of Warcraft) but the ARPUs had been 75-90% lower. Then Activision Launched Call of Duty Mobile and the ATVI numbers shot up like crazy. However, the incremental MAUs have again translated into an ARPU that is at least 75% lower than desktop/console.

The good thing is that mobile ARPU is growing. Historical ARPU growth for most publishers has exceeded 100% over the last 5 years. Further, based on my conversations with major publishers, less than 10% of the user base of a free to play game is ever monetised and a small set of “whales” account for nearly 80-90% of the revenue. As old franchises with huge user bases like Hitman, MGS, Call of Duty and PUBG make their way to the mobiles, ARPUs will only increase.

Next, we talk about monetisation strategies

3. New Monetization Strats

If you are as old a nerd as I am, you probably remember the terms freeware and shareware. Hold on to this one for a moment. Historically, video games have cost anywhere between 40-100$ and you would typically get everything on the media (CD, DVD, HP Tapes). Then, the internet rolled around and while multiplayer gaming got better, it also allowed the publishers to gouge us again via the shitty shitty innovation called the DLC1. Think about it, kids don’t have money anyway. Then these jackasses at the publishers keep releasing new stuff like new character clothes and relying on FOMO to make the sales happen2 - So you have this hybrid model where you have managed to create a recurring revenue even after having charged full price (does this remind you of NFTs?).

Eventually, some genius had an idea - why don’t we make the game itself free to play (F2P) and charge for the DLC. Anything that makes you a competitive player will be charged - and the vanilla game will be tweaked so that maybe 20% of the players can do well using the free version only. Anything else you need, a powerful gun, healing kits, building materials - everything is paid via in-game micro transactions (MTX). Sure, you can grind your way acquiring these items but you can simply buy them for $0.5 and isn’t that just easier than doing some repetitive shit for 3 hours? Even the dances your player does have to be paid for3.

Most DLC sales used to be gameplay related items - missions/maps/modes. Today, more games monetize by selling cosmetic items in MTX that don’t impact multiplayer gameplay, like skins in Warzone or Nike Air Jordan’s in Fortnite.

Now, it’s easy to see that people would leave a platform where you quite literally have to pay to be a competitive player fairly quickly after being knocked around. And that happened. e.g League of Legends was usually a very niche game and did not have a large following. Then Fortnite came along in 2017 and things changed. See, this tweaking of gameplay I described above in the previous para is an extremely hard thing to do. But, Fortnite somehow managed to get it right. Their innovation was the Battle Royale - an adaptation of the 2000 Japanese movie where ~100 players fight with each other. The prospect of shooting your friends in the face all day has been so powerful that Fortnite typically has >300mn MAUs and an ARPU of ~$15 per player. Insane right?

EA took it one step further and basically turned it into a pay to win model. If you want to play Need for Speed online, you need to pay to build a reasonably competitive team. Sure, its downright filthy and scummy and someone at EA should die of rectal bleeding, but it’s incredibly powerful and profitable.

How profitable?

Should you want to make your way to the latest financials of EA, TTWO or ATVI, you will find that in-game txns (i.e DLC or MTX) accounted for anywhere between 40-60% of their total revenues. No negative impact, no cannibalism, pure value accretion.

Now, the incremental development cost to create new game content is pretty low. Operating margins are much higher (because you are often directly buying from the publisher). As this trend continues and the DLC/MTX revenue contribution grows, margins will continue to expand.

Think of F2P as a removal of barriers to entry. Earlier, you needed to pay a steep entry price to play a game. Now you can play it for free. and F2P components of paid games (like Warzone) can lead to upsells from players who may now want to buy the paid game itself (in this example, Call of Duty).

So, Shooting friends is fun and a moneymaker. How about competing and shooting strangers?

4. E-Sports and Streaming

If someone told me in 2010 that people would spend hours watching other people play video games - I would have asked what they were smoking and then, if I could have some.

For the 2021 League of Legends world Championship - 30mn people showed up to watch. In 2019, that number was 4 mn. In contrast, the IPL 2021 final had a viewership of ~11mn. I couldn’t help but let out a long, low whistle as I looked up this number.

But much like IPL, video games can be monetized. People have YouTube channels where they play games and people watch. One of my favourite Streamers is Aculite - he has ~1.2mn subscribers. in 2016, ATVI sold the rights for the Overwatch League to Twitch for $45mn for two years. Twitch was subsequently acquired by Amazon for a ~$970mn. Anyway, I digress. When the Twitch contract expired, YouTube agreed to pay $54mn for Overwatch and new CoD League. Now, these are nowhere near the prices paid for IPL but if the viewership keeps growing like this - that day isn’t too far off.

Now, much like the BCCI, the league owners (in this case, usually the publishers) are also able to sell teams. For the 2017 Overwatch league, ATVI sold 12 teams at $20mn each. That has now expanded to 20 teams. Not a bad payday eh? Now, while this isn’t exactly chump change, it is a nice one-time revenue for ATVI. What is interesting is the people who have bought these leagues. Robert Kraft and Mark Cuban own teams. American Football, Basketball and Video Games. Ah well….

Then there are sponsors. League of Legends sponsors include Mercedes, Spotify, Mastercard and Bose.

5. Social Gaming

There is a beast that didn’t exist when I was a kid, MMOG. Very quickly, MMOGs are what Ready Player One’s Oasis will likely look like if it were real. This is also a driving trend behind the emergence of all kinds of NFTs and DAOs - a lot of the content is related to gaming.

First we had multiplayer on consoles. So Xbox players playing HALO multiplayer with other HALO Players on other XBoxes (typically 2-10). Developments in tech have allowed for Cross Platform play so PC gamers can play with console players (and PC players using mice tend to wipe the floor with console gamers).

Next has been the rise of Battle Royale games - so 100+ people are playing together (imagine the technical complexity of making this work).

Today, Games like Roblox allow you to create content - and open the door for the average gamer to make money off playing games ala Instagram influencers.

All of this stuff contributes to the formation of communities, and communities create loyal fans and players. That loyalty creates a real switching cost for a member of that community. If a Call of Duty player has a favorite Call of Duty streamer, a group of friends that they play with online, and has spent money customizing their online identity, it’s unlikely that they decide to all of a sudden change gears and commit to Overwatch or Battlefield. Here is an excerpt from an ATVI press release:

“We recently received a heartfelt letter from a Call of Duty fan in Ireland. He wrote to us explaining how he and three school friends had stayed in close contact by playing Call of Duty even as they went to university, got jobs and moved around the world. He talked of the bond that they forged over many hours of gameplay over many years, and how in turn his mother would see the enjoyment and warmth that he felt from spending time online with his close friends. When his mother was tragically killed in March this year, those friends traveled long distances to be by his side and comfort him, making him forever appreciative of the strength of the friendships forged through years of enjoying Call of Duty together. They remain in touch through the social experience of playing Call of Duty.

Stories like this are a powerful reminder of how our titles can impact, inspire and unite people around the world, empowering them to achieve amazing things through their shared love of gaming. Although we have only just started to scratch the surface of what’s possible for social networking around our games, we are already connecting people around the world in extraordinary ways. We are committed to exploring innovative ways to bring our players closer together, further deepening the experience for communities and in turn widening the moats around our largest franchises.”

I also have a paper for you to read here which explores this social dynamic in more detail.

For a publisher the benefits compound - there is zero customer acquisition cost for the next iteration of the game, and potential for higher ARPU via MTX. And, as a total side benefit, an incredibly robust moat. Try selling another game to a CoD player.

As always, network effects often create the strongest moats.

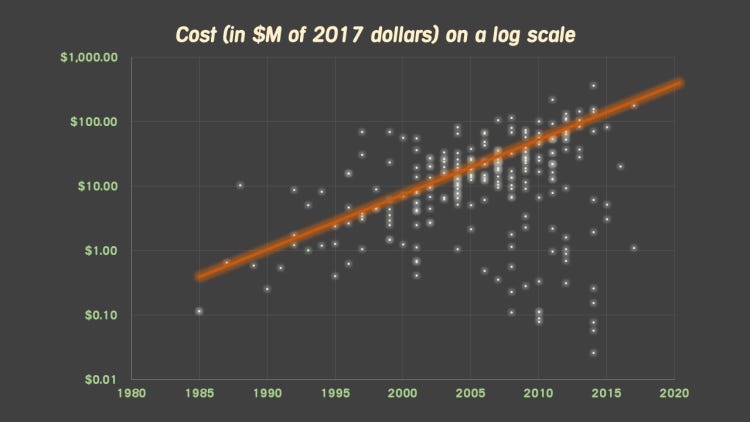

6. Pressures on the Industry

In 2018, Ralph Koster wrote a very well researched piece on the rising costs of game development. He used data from some 250 games from 1985 to 2017, using private data from his industry contacts. Key takeaways:

Sizes of top titles have increased like crazy. Chart below is on a log scale.

Cost per MB (if such a metric makes sense) has fallen but the overall cost of games has increased.

There are significant entry barriers to this industry for new publishers or indie developers. In real dollars, the price of a game has fallen by roughly 50% from 1990, despite the increase in development costs. So, margins are compressing. What this really means is that it is really difficult for non-incumbents to break in - i.e. a remarkably deep moat for the incumbents.

New hardware almost always leads to a price increase in games. Most publisher balance sheets get shot the moment a new console lands - because everything needs to be written from scratch and you cant really charge people to whom you sold a game on PS2 again for the PS3 version4.

Please do read Koster. He writes well and this data presented is not really public.

7. Demographics

Media consumption habits can be formed at an early age and can be very sticky. As an example, I would any day, rather read a book than watch TV, because my TV usage was very heavily restricted when I was a kid. Sure, paper has been replaced by a kindle, but the song mostly remains the same5.

The point I am trying to make is that someone who grew up without video games is very unlikely to pick up PUBG in retirement.

The first coin-operated video arcade game, Computer Space, was introduced in 1971 - nearly 50 years ago. Nintendo released their first console in 1983 (37 years ago), Sony released the first PlayStation in 1994 (26 years ago), and Microsoft introduced the first Xbox in 2001 (19 years ago).

Somebody who is 50 years old today would have probably dabbled with video arcade games, but would have been in their mid-20’s when the first PlayStation was released - they were unlikely to become a video game enthusiast. On the flip-side, someone who is 36 years old today6 has absolutely grown up in an era of serious console gaming, and is much more likely to have played console/PC video games as a kid, they probably still enjoy playing video games today, and they will continue gaming as they enter their 40’s, 50’s, and 60’s than people that age today7.

Now, it is difficult to guess how video game consumption for a given age cohort might change as gamers age, but I think that gamer penetration in older cohorts will be much higher in the future than it is today. And that is only going to be a good thing.

Alright then, this was a deep dive on the VIdeo Games Industry. There is a lot I didn’t cover - VR games, gamification - but this was intended as a look at the video games of old, a love letter to the past.

If you have questions, please do send them to me. Feedback is always welcomed.

Downloadable content

Yes, I was one of those kids and that asshole from EA who decided to make FIFA mobile a MTX Platform will one day be castrated by me. With a blunt spoon (Sorry, too much Dexter).

And Fortnite stealing credit for creators is a whole different topic worthy of a Netflix episode. Wait, they already did that.

Actually, you can, and people have tried, but the retribution and cancelling has been swift and merciless. Never fuck around with a crowd of nerds. They will stab you with their spectacle stems. In the eye.

Led Zep reference for old folks.

Ahem!

Amen!