Crypto #1 | Understanding Crypto, DeFi and NFTs - A Primer

Crypto #1 | Understanding Crypto, DeFi and NFTs - A Primer

I am not sure I understand it all.

The "Writer's Block" has continued for this non-writer. So I thought instead of trying to dive deeper on 100x EBITDA multiples, I will rather write on a highly technical topic and make it layman friendly. Put that Computer Science Degree to some use.

One of the things I end up constantly explaining to people is Bitcoin and Crypto. So this post is mostly me making a resource that I can send to folks to spare me the same conversation, ad infinitum, ad nauseam. None of this is new ground or original thought.

Caveat - this series on Crypto is written with the layman in mind. Should you want to have a discussion on technical aspects, the impact of the London Fork, Beacon chains and other such, please reach out to me directly.

OK, disclaimer done. Here we go with the first note.

1. Basics

Historically, computers (and hence, Computing time) were expensive, scarce resources. Then came the IBM 360 and the era of the Mainframe was born. For the next 30 years, technology galloped, but the best way to create a network was to have the scarce computing resources in a central repository and have relatively cheap access devices spread out to access this centralized computing power. Everyone submitted their requests for computing time and the computer took them up basis priority and load. So, there was always a pipeline of things for the central computer to do and its incredibly expensive time was not being wasted. The terms Client and Server have their roots in this age. We'll leave this context here - an entire set of books can be written about the exceedingly fascinating history of computing. AMC's Halt and Catch Fire is a great show about it, should you be interested.

The first thing that we should understand is Distributed Computing. Most people reading this are likely my age so they may remember SETI@home and Folding@home. These were highly computational projects which were strapped for cash. So they requested folks whose desktops weren't used that often to lend some of their spare computing power to solve the computation problem. The key advance here was breaking the problem into MECE style blocks that each node in the network could solve and send the results back. Think of it like a boss assigning work to underlings and then arranging their results into a cohesive whole.

Distributed computing still was a client-server model. If I were to take out the server, everything else would simply shut down. The next advance was Decentralized Computing. Each application runs simultaneously on multiple computers which are talking to each other to solve a problem. If i were to take down a few of the nodes in this network, the application will carry on just fine, albeit with reduced resources (and hence, speed). Best example of this is P2P networking - e.g. BitTorrent sites. There is a reason why they have been incredibly hard to kill off.

Blockchain was created as a way to create a permanent record that could not be tampered with and which was widely available. Each Blockchain consists of blocks which are linked together via Hashes. Basically, each new block has encrypted data in it about the previous block. So, changing anything later is very difficult and almost impossible to pull off. There are also multiple copies of the blockchain which MUST agree, so even if you changed things in one blockchain copy, it is extremely expensive and nigh impossible to make the change everywhere. So expensive, that even nation states cannot afford it. The name Crypto comes from these encryption hashes.

The underlying problem for trusted blockchain is a very simple one - how do decentralized parties arrive at a consensus without relying on a trusted arbiter. Or, to put it another way, When I cannot verify the identity or reliability of everyone else on the network, it is still possible to collectively agree on a certain truth? Here is a link to a paper from 1982 on the byzantine generals problem which is effectively the same question.

Ok. Basics Done. Next - Cryptocurrencies.

2. CryptoCurrencies

CryptoCurrencies are virtual currencies. They have no physical form, they operate on a P2P Basis, they are trustless, permissionless and they have limited supplies. The most prolific ones are Bitcoin, Ethereum, Binance and Tether.

Bitcoin was revolutionary because it brought together two relatively new but proven concepts with a a game-changing idea solving the trust problem outlined above. Effectively, we can break Bitcoin into 3 components - P2P + Blockchains + Proof of Work Consensus. It's a zero knowledge proof and while I won't go into the mathematical underpinnings of this beyond a point, here is the gist - miners validate transactions. Each new linked block is a representation of the work done to validate a transaction. By definition, the chain with the most validations is the longest chain - and the longest chain is most valid. Miners are incentivized to not muck around and stick to the longest chain because no one will pay them for results that don’t agree with everyone else. All of this coalesces into agreement on the longest ledger by proof of work. Here is a great video from 3Blue1Brown (one of my favourite youtube channels) about it. For the more technically minded, here is another, very accessible writeup by Michael Nielsen.

Bitcoin was originally a solution looking for an answer. It started off as a P2P cash alternative. But because of the nature of the blocks themselves, it also has the ability to act as a verification mechanism. You could verify identities, transactions, title deeds - pretty much everything. Now, this ability - of transparently, publicly verifying identity data - is extremely valuable. This brings us to the second generation of blockchains - Ethereum is the most prolific of those.

However, Bitcoin has a deep conceptual problem - it is not Turing Complete. Once again, it’s a highly technical aspect, one we won't dive into, but it boils down to this - Bitcoin is optimized for storing value, and it excels at transfers. That's it. Ethereum and later currencies were designed to be broader. They allow for smart contracts and are highly programmable. Another way to look at it is this - if Bitcoin is the HP12C, Ethereum (e.g.) is Wolfram Alpha. Another way to look at it is the use cases enabled - Ethereum (e.g.) is highly transactable and is exchanged fast. Bitcoin is mostly HODLed. A great but technical writeup on how Ethereum works is here.

Now, we need to take a small detour to understand Smart Contracts. Here is a very nice video about it. Effectively, a Smart Contract is an automatically executing, unchangeable agreement. If this happens, do that. No discretion, just the cold logic of a machine following instructions. The original idea paper by Nick Szabo can be found here. Highly recommended read.

As an example, here's how it works when it comes to Ethereum - a programmer will code the smart contract using Solidity (which is the Ethereum programming language), upload it to the Ethereum system. Then, everyone of the nodes get a copy of this contract for verification. Once all nodes have verified and agreed on the outcome, the transaction is added to the Chain.

Now, all this validation and consensus verification costs a lot of effort and energy, so Cryptocurrencies will pay the people who do this (called miners) for this in the form of new supply. This is usually the only way for new supply of Cryptocurrencies to come online. e.g. Ethereum will pay the Gas fees - which will compensate the validators for their electricity, effort and infra.

One last thing - the monetary logic of cryptocurrencies is quite complex and varies, but over time, it is either capped or deflationary. The supply is either constant or goes down over time (in relative terms) e.g. Bitcoin follows halving.

Lastly, of all the cryptocurrencies, Ether is closely tied with DeFi (more on that later) - it is used as the reserved asset, the unit of exchange and as collateral.

Next - DeFi.

3. Decentralized Finance - DeFi

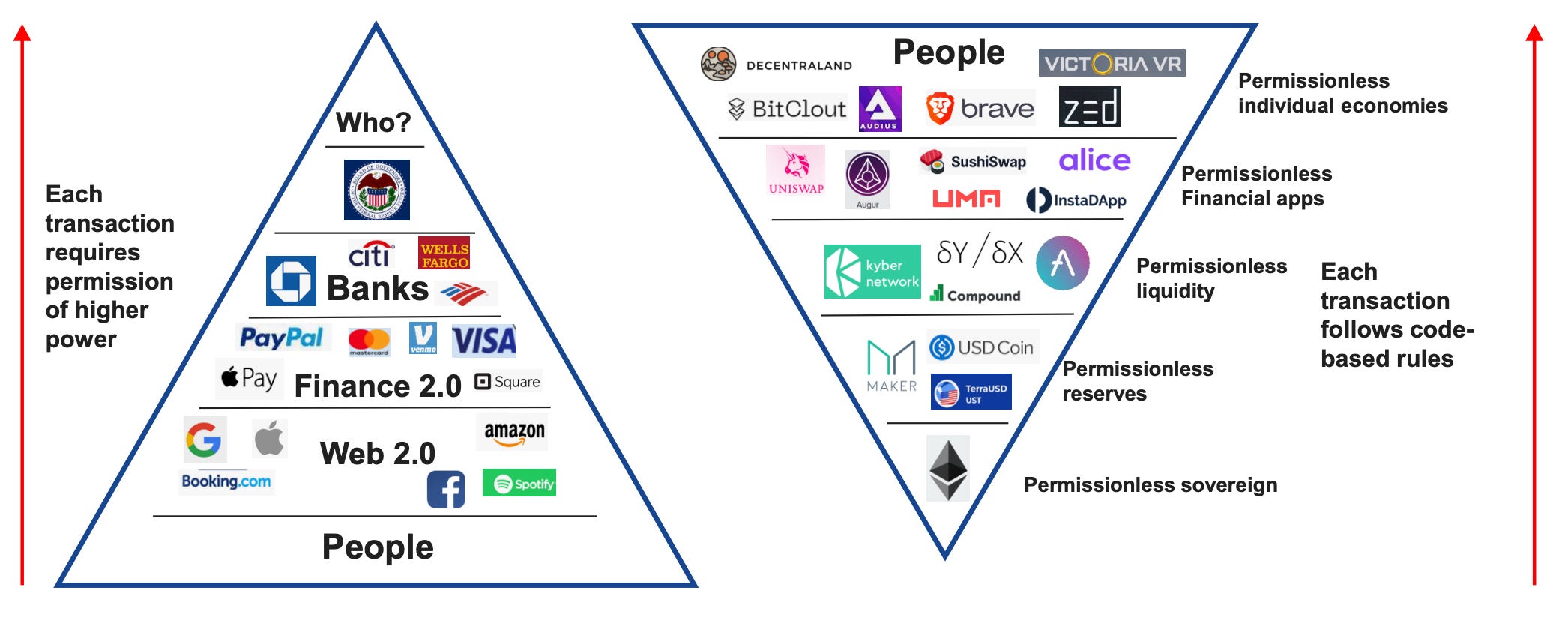

DeFi is an ecosystem of financial applications, built on the blockchain / ethereum stack. The common thread running through them is that unlike the real-money economy which is based on institutions and therefore centralized, the DeFi apps (dApps) are completely decentralized. Because there is no central resource / enabler, these are not easily blocked, and are available all the time. Here is a useful graphic to visualize this1

Here's a more detailed look at what DeFi offers that the traditional finance institutions don't:

It is Permissionless - so it offers a parallel channel to institution controlled banking infrastructure. This is a good and a bad thing. There is a reason why almost all ransomware funds are transacted in bitcoin. There are no (theoretically) barriers to entry like KYC - you won't be requiring an Aadhaar card to open a Bitcoin wallet.

It is Interoperable - as long as I have ETH - I am sorted. there is nothing else really needed to do the most complex transactions. Sure, I may have to convert ETH to DAI (another cryptocurrency) but there isn’t really a whole lot that I cannot do in terms of financial services with Bitcoin/Ether.

it is Self Regulating - Fraud is very hard to do as long as the keys are protected. Inflation is heavily controlled as the supply is capped or declining over time. It's hard for someone to misuse your money (e.g. speculative lending by a bank) because the money is always under the owner's control. The entire system is transparent - you can look at the data and code and see exactly how it works and what checks and balances are built in. My money in HDFC will be lent out by HDFC. If my money is in the blockchain, I will be the only person who decides if it gets lent out.

The biggest difference with DeFi is that it does away with the concept of too big to fail. It effectively disintermediates the Centralized financial institution model.

However, there are also some significant problems with DeFi (as it exists today). Scalability of the underlying blockchains and time needed to validate transactions are choke points. There are scams and hacks (but these can mostly be traced down to human errors). It also, does not play well with financial regulation today (e.g. hackers and Bitcoin ransom demands that cross borders very easily).

At this point, you may want to ask me this - How is all of this any different from cash. If you don’t want your cash lent out - keep it under the mattress. Whats the need to go through all these hoops? The answer is that it isn’t different. Any currency is only valuable if it has credibility. There is a reason why too much money printing leads to devaluation - each incremental bank note is in effect an incremental erosion of credibility. the Rupee has value because the RBI is credible and backed by a sovereign. And it doesn’t operate very differently from banks either. Banks pay depositors interest to use their funds to lend out. In the Crypto world, you can (e.g.) stake your Ether and receive fees for securing the protocol (~5% annual today). Not very different from savings bank accounts.

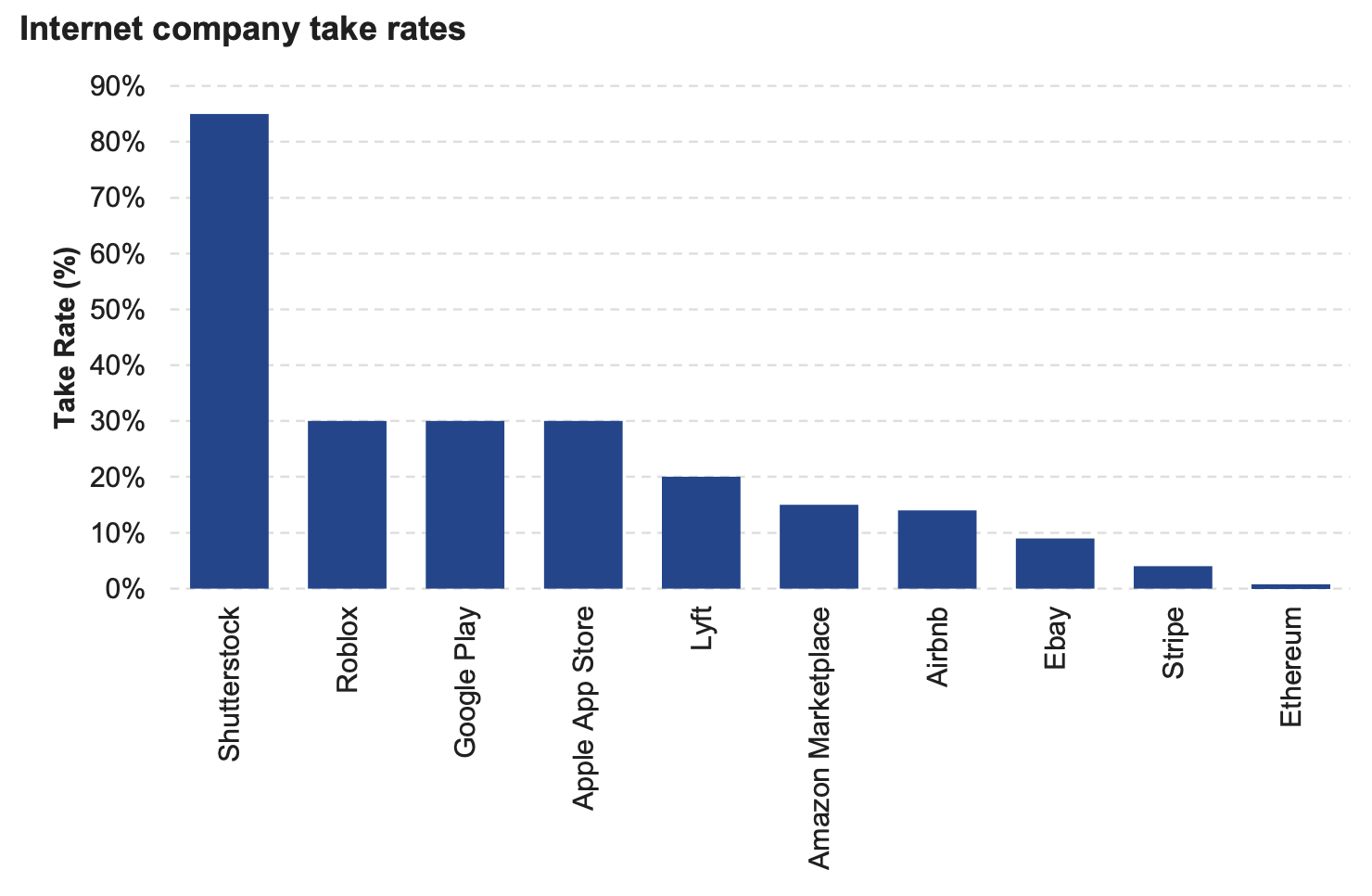

At the heart of the DeFi movement’s viability is a deeply capitalistic motive - Costs. DeFi costs far less. The average operating cost to income ratio for Indian banks is ~45%. For US banks, it is as high as 60%. For DeFi - it is less than 5%. If you really don’t need employees and if the work is being done on scale by a machine, why would you need to pay 50% of your income as costs? What this leads to is lower rent seeking and therefore lower costs for users. If we were to look at Ethereum as an internet company, its take rate is lower than anything else comparable2.

There is another beast called StableCoins, which are nothing but cryptocurrencies pegged to a fiat currency like the USD. Tether and TrueUSD are great examples. They are likely also the first ones to get regulated and hence mainstreamed - given the crossing-over to the real world they offer - without the volatility.

DeFi is still early - we are still figuring out the protocols, the use cases, the trust pitfalls, the scams, regulation and so on. However, in the long term, Cryptocurrencies are likely going to be the models. What may be likely is that the central banks themselves start issuing Cryptocurrencies.

Next - NFTs

4. Non-Fungible Tokens or NFTs.

The name pretty much explains everything about it to us. Non-Fungible Tokens are an encapsulation, an abstraction of digital assets onto the Blockchain.

Tokens are programmable blockchain assets. They can represent money, Paintings, digital art and so on. Ether is a token, Bitcoin is a token. Ethereum and Bitcoin are fungible tokens. One bitcoin is same as another. NFTs are not fungible. Each represents a unique asset. e.g. there is only one Mona Lisa. The underlying art may be copied (e.g. photos of the Mona Lisa) but the ownership remains with the NFT owner (in the real world example, the Louvre).

Now, for the most part, NFTs have been a distraction (except for creatives who are able to see true disintermediation, but that’s a whole different discussion) for the most part with in-game items and questionable digital art. Elaine Ou has a brilliant and funny writeup on breeding digital cats here.

However, this does have significant real world applications. As an example, think of the problems with Land Records in India. Now imagine instead of registry papers, you are issued an NFT. Anyone can verify who owns what - and ownership is unquestioned. Prospects for frauds are reduced e.g. in case of a sale because it is done via a smart contract. Taxation is easy.

Other use cases include patents, IP, supply chains, bill discounting, contract enforcement, tracking counterfeits and so on. Even academic degrees and certifications would make a great NFT use case.

5. Crypto as an Asset

For me, the crypto asset class has matured significantly. The first code (Bitcoin) started running in 2009. Since then, liquidity has increased sharply, it has survived 3 bubbles, there is an active F&O market and retail participation is increasing steadily. In Feb 2021, liquidity at the largest exchanges was as high as $25bn in avg daily volumes. A couple of years ago, this was only about $7bn.

Here’s a more sobering thought - Bitcoin’s market value at ~$900bn is higher than India’s M2 money supply ~$700bn. It behaves similar to gold and is in fact, being used as a proxy for precious metals as a store of value.

However, will strongly recommend that unless you know what you are doing, don’t get your money trapped in crypto trading. The risk and volatility are too high.

Source: Van Eck (https://www.vaneck.com/us/en/blogs/digital-assets/ethereum-bull-and-bear-case.pdf)

Source: Van Eck, The Block and CoinMetrics