VC#16 - Is Cash a Moat?

VC#16 - Is Cash a Moat?

second post on cash - arguing the other side. ish.

Hello!!!

Yes, I have been away for some time. Mostly it has been spent travelling, dealing with cameras (wanted to switch away from my D750 but mirrorless camera EVFs are just not for me). More importantly, there wasn’t really much to write about. Here is the most interesting stuff if you ask me from the last 3 months:

We landed on the moon. I won’t resort to jingoistic shit but the scale of the achievement is hard to put in words. A wee little 27 kg robot. We lit a (literal) bomb under its keister and the little man zoomed off into the heavens. Then we saw this image:

Rahul Yadav topi-pehnao-ed Naukri inc. I am told FIRs have been filed. Caveat Emptor, anyone?

Pawan Munjal was raided. 25 crores of assets were recovered. Chhatarpur junta sniggered at the relative pauperness of the haul1.

Zomato became profitable (cough cough deferred taxes cough cough).

Now, for the main programming - Have you watched Daliland yet? It is not a particularly good movie but it does have some trippy moments. The whole movie builds to a 10s sequence when a main character realizes that they are really screwed because their source of inspiration is gone. Denial was a necessary part of feeling like a winner.

Sounds a bit like start-up-land eh?

¿Qué hay en un foso?

Or, what is in a moat, really? Well, VC types like I would use the term “Moat” to describe a competitive advantage. It may be defensible, it may be differentiated. It is anything that sets winners apart from the also-rans. It is anything that allows one to maintain market share and/or profits.

Is Cash a Moat? Is it differentiated? Is it defensible? Is it something that allows one to maintain market share and/or profits?

I think we can all agree on one thing - Cash is a lifeline. Expressed as a formula -

Cash in the bank = inevitability of survival.

Does that also equate to inevitability of success? In some cases, Yes. It depends, really. Now, you may say - what BS. But bear with me. There are cases when burning cash works as a moat.

Is all Cash spending equal?

Building businesses is hard. The Red Queen quips in Through the Looking Glass:

"It takes all the running you can do, to keep in the same place."

I think the point I am trying to make is that there are no sure bets in building a franchise. You can have the smartest people, the most advanced tech, crazy tailwinds and unlimited TAMs, both Tiger and Softbank on your cap table (and hence, unlimited capital) and still fail. You can also have a crazy idea and an old Pentium III and still be wildly successful.

Cash then, is only a part of the equation.

Now, I have been bouncing from place to place in private markets for 15 years now. When you look at companies which sucked up a lot of investor capital floating around, you see some interesting patterns emerge. Cash is only an advantage when the underlying market dynamics, maturity, execution and unit economics make sense. Cash itself can be a steroid for the dedicated and the disciplined, but in and of itself, will often lead to shrunk testicles.

There are two things that set the companies that made good use of high cash raises vs those that royally screwed up:

Mindset - your relationship with your cash reserves

Metrics - what you choose to prioritize in terms of outcomes from the cash at hand.

Mindset

The best founders, and especially the ones who create value are paranoid about cash. A lack of Paranoia is strongly correlated with implosions. Allow me to illustrate:

Remember Wework?

It was a wonderful company which brought to us such gems as community adjusted EBITDA. It collapsed simply through the act of filing an S1. Wework released its S1 to a positively bewildered2 public in Aug 2019. It had raised $12bn in funding and was valued at $47bn. The fall was spectacular. The CEO stepped down in September, Softbank took control in October, Wework laid off 2,400 people in November. Today wework is a publicly traded company valued at $262mn.

What shocked the world was an insane attitude towards money - burning $2bn a year in cash, "community-adjusted EBITDA", and the CEO claiming “energy and spirituality” as the most metrics for its potential in public markets than measures of its revenue and losses. Bad relationship with money and no paranoia.

But we could claim that Wework was an aberration. Let me provide you with another example.

Have you heard of a company called Fast?

In November 2020, Fast was 18 months old and they were raising money. Funnily enough, they had a person selling swag before they had a product market fit.

Now, they ran trying to raise as much as they could because they thought they could “close a round on favourable terms due to conditions in the VC market”. Stripe led a $102mn round in January 2021. This was by most accounts a purely opportunistic fundraise - without a viable product or customers.

That overconfidence led Fast to grow their headcount to 500 people and a $10mn a month burn. At $600k in revenue, it worked out to $1200 per employee. Cash bonfires took the form of $150k+ retreats in Honolulu and Denver and corporate coaches who worked with professional athletes.

And in one of the recurring examples of markets standing in for Mike Tyson’s artillery strike of a right hook, Fast got punched in the face. Its competitor Bolt on the other hand raised a much smaller round in spite of having a revenue 50 times the $600k that Fast had. Fast forward to August 2022:

My point here is that spending cash has to be done with a strategic mindset. It isn’t about frugality. It is about extracting maximum juice from each dollar spent. Effectiveness of spend has to be measured. If hiring a private jet leads to a measurably better business outcome, by all means go for it. Which segues nicely to Metrics.

Metrics

If you are a bit of a nerd like me, there is a lot of fun to be had looking at P&Ls. But then, I have always found the most interesting thing about any company to be its cash conversion cycle. Companies are engines. They are supposed to take a small pile of cash in and throw a large pile of cash out. This has to do with margins and revenue conversion - sure, but also the efficiency and optimization of operations.

Cash conversion is a fascinating and powerful analysis tool. It is a highly effective way to do apples to apples comparisons of businesses. If the ultimate purpose of a business is to eventually generate reliable streams of cash flow, then how effectively the business takes in cash and turns it into more cash is a key question to ask.

A great read on this is Jay Vasantarajah’s analysis of Gymshark. Gymshark has a negative cash conversion cycle. Closer to home, one of my portcos - Thyrocare had a negative cash conversion cycle.

The Cash is a Moat Narrative

If you talk to people, you will see that the whole “cash is a moat” narrative inevitably comes up in the context of sectors which are thought of as “winner takes all”. A lot of these have been in consumer markets (food delivery, hyperlocal, ridesharing) where companies are racing to build new behaviours with the hope of monetizing down the line. I argued in a previous post that cash has become heroin - the last few years’ bull market is when the addiction to cash really spread far and wide. Let me pose 3 questions:

How did the players in specific industries treat cash?

Did that cash convert into a competitive moat?

How did the cash impact the ultimate outcomes?

Allow me to present a few case studies:

Enterprise Software: Snowflake is a great example of a historically egalitarian sector being tilted when loads of cash are thrown in. Snowflake raised ~$1.5bn in funding. They burned about $200mn to get to about $100mn in ARR. And even though Snowflake’s business has low margins, their business is a great example of maximizing juice from cash spending. Snowflake is a very, very sticky product. It sits at the infra level - one where people are loath to rip out something that works. What that translates into is very few alternatives to Snowflake. Usage based pricing leads to an insane retention of >150%. What that means is that Snowflake can afford to spend $150k to acquire a customer that will only net $50k initially. Why? because the customer will grow 2-3x in size next round. This isn’t a light money on fire dynamic. They are a very unique business where spending money to quickly get your teeth in makes sense because of stickiness, upsell potential and technical leadership.

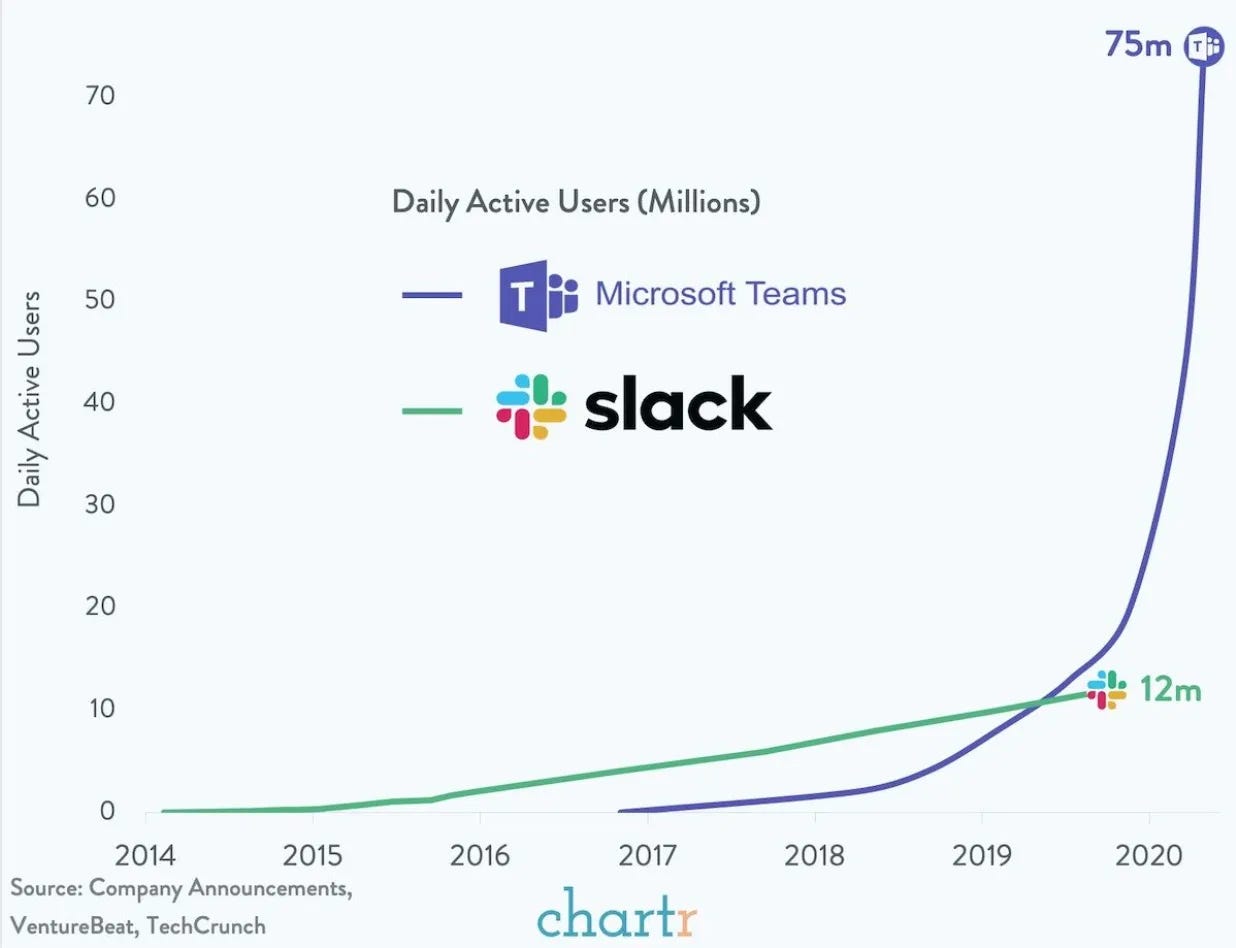

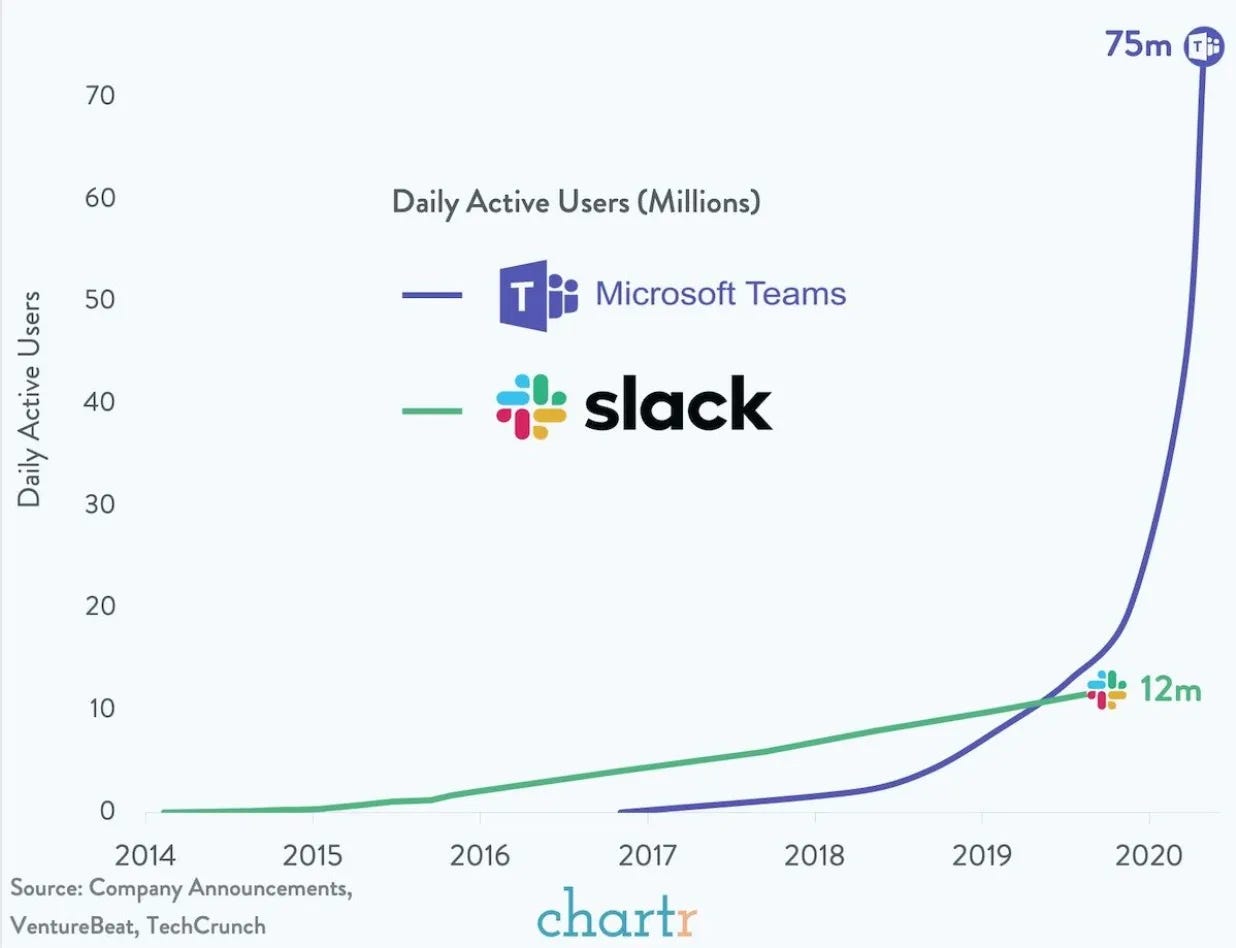

Productivity Software: Productivity software really reminds me of the food delivery business. Productivity companies spend a lot of money acquiring customers, often for low initial revenues. Even though they have strong bottom-up momentum, they are incredibly similar to Swiggy and Zomato. They spend like crazy building market awareness. They point to grassroots momentum and Ubiquity as moats. But think about it. Are they really sticky like Snowflake? I mean Sure, notion is great, but is anyone using Notion in a way that makes it a core part of their stack? Not really. It will be ripped out when something better comes along. What happens when these companies stop spending on marketing? The next tool comes, pushes for the awareness share and eats away at their business. Sure, huge amounts of money have been burned in marketing but has that translated into a moat - not really. What is the real moat? - Distribution. Here is a chart. This picture is indeed worth a thousand words:

Ride Sharing: The original “cash war” sector. Loads of competitors. The companies that survived were the ones able to raise cash most effectively. It has played out between Lyft and Uber, and it played out closer home between Ola and TaxiforSure. TaxiforSure died because of adverse news environment, not because it was a bad business. It was certainly more efficient than Ola. Everyone spent the cash on marketing and acquiring customers. Scale played an important role, Cash reserves did indeed play a role in terms of determining who survived. TaxiforSure died because it’s fundraise coincided with an adverse news environment for ridesharing in India - it was a far superior business than Ola. Cash indeed worked as a moat here

Pulling it all together:

I would argue that the smart entrepreneur will do themselves as many favors as possible in finding components of their product or market that work as natural moats. Cash can help us build any number of those, but it's important to understand when burning to build a moat is the right call.

I would argue there are 4 reasons to leverage cash to help build a moat:

Building new behaviors: Rideshare and food delivery cos were pushing to get users to develop new behaviors. If you can own a market and become the solution people associate with that behavior there could be inherent customer loyalty in that. However, I haven’t seen it play out. Ever.

Unit economics at scale: Some companies see their unit economics change at scale. In such cases, getting to scale quickly makes sense.

Stickiness: Typical double edged sword. It can work for you if you get there first, but it will work against you if your competitor is already there.

Massive expansion: When you know a customer will naturally expand with your product (e.g. more usage with Snowflake or more payments with Stripe) then it makes sense to burn to get into those customers so that you can grow with them.

There are also 4 reasons to be cautious of leveraging cash to build a moat that may not be sustainable:

Lack of defensibility: The reason application software often struggles to have a meaningful moat is because the differentiation is mostly in the interface. UI is not a long-term competitive advantage. Here’s looking at all ChatGPT wrappers.

No platform advantage: If you are still chasing supply and demand even when at scale, better to be frugal and highly deliberate in terms of spending.

No distribution advantage: Think of Microsoft being able to use Windows to push Teams. Or Uber being able to launch Eats with their existing driver network. Open source or product-led growth can certainly be distribution advantages but they're rarely a long-term defensible moat because they're available to everyone.

Limited upsell opportunities: Every company has to have a viable argument to explain why their product can progressively become more important to a company. If you do not have visibility and evidence on upsell/Xsell potential, wait.

There will always be the “move fast and break things” people who want to raise $100M every 6 months lighting money on fire as they go. And there will always be the bootstrapped worriers who look at VCs as parasites who ruin businesses. Neither of them will always be right or wrong. Cash, like any strategic asset, is a double-edged sword. It can be used effectively (even in large quantities) or it can impale you. All I would say is that there are times to be circumspect, and there are times to go all-in.

Interesting Reads:

Pershing Square letter. Great read on macro and hedging.

Cost of Raising Children in India. It’s expensive.

Housekeeping:

As always, I look forward to hearing from you. If you liked this post, pls feel free to share this or subscribe to this newsletter using the links below. While I have been tardy of late, I try to write a 1000-2000 word essay once every 4 weeks or so.

A chhatarpur friend deadpanned - “sirf 25 crore? gareeb nikla bhai toh.”

Gobsmacked just sounded a little too flippant. I don’t know why.