VC#15 - The Venture Capital Model is broken.

VC#15 - The Venture Capital Model is broken.

When Risk Capital becomes Heroin.

Hello!

This essay has been in the making for a couple of years now. This is more of a manifesto so if you see something that seems particularly extreme or militant - please, bear with me. And please do feel free to tell me if I am getting this wrong.

Dramatis Personae:

The world of investing has 3 key players:

Owners of Capital (LPs)

Allocators of Capital (GPs)

Transformers of Capital (investees, in this case Startups).

The motivations of these 3 constituencies are pretty transparent. Owners of Capital want to maximize their wealth, Allocators want to minimize risk and maximize their share of returns / fees, Startups want to generate superlative shareholder returns.

In practice however, Owners of Capital are often conflating wealth maximization with risk taking, Capital Allocators are trying to deploy capital at hand as soon as possible to raise the next fee-generating pool of capital and Startups are looking to grow and chase valuations instead of focusing on long-term value creation. Provocative statement? More follows.

Unsustainability is a feature of young businesses:

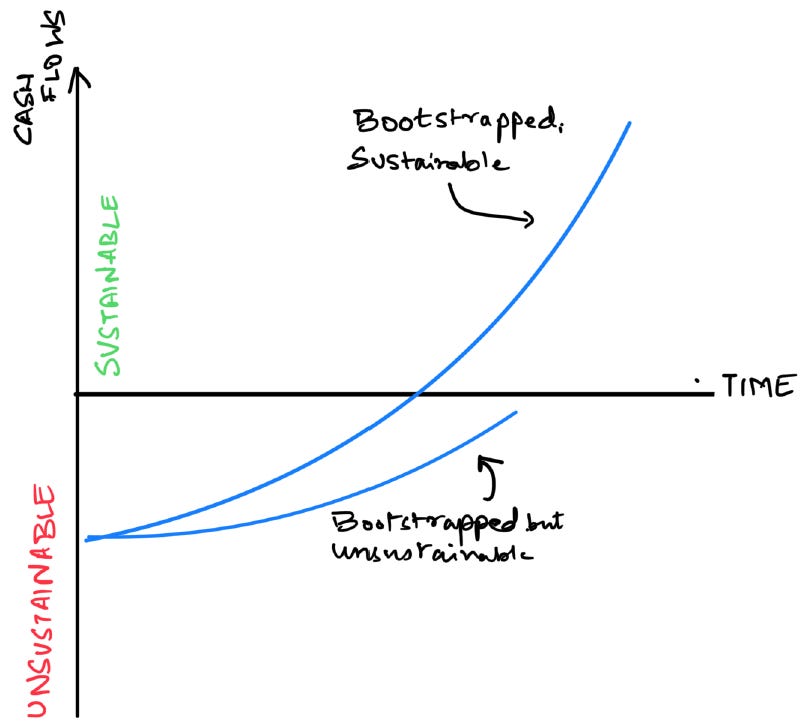

Think of any business you may be familiar with. It took time for it to become profitable and get to self-sustainability. No business can be cash flow positive on Day 1. This is why, for more than 3000 years of human history, entrepreneurs have always had raise funds. The trade-off is very simple. Initial funding helps sustain a subscale (hence, unsustainable) model in favour of eventual sustainability. This runway is critical for building any business.

The two outcomes for a bootstrapped business can be graphed thus:

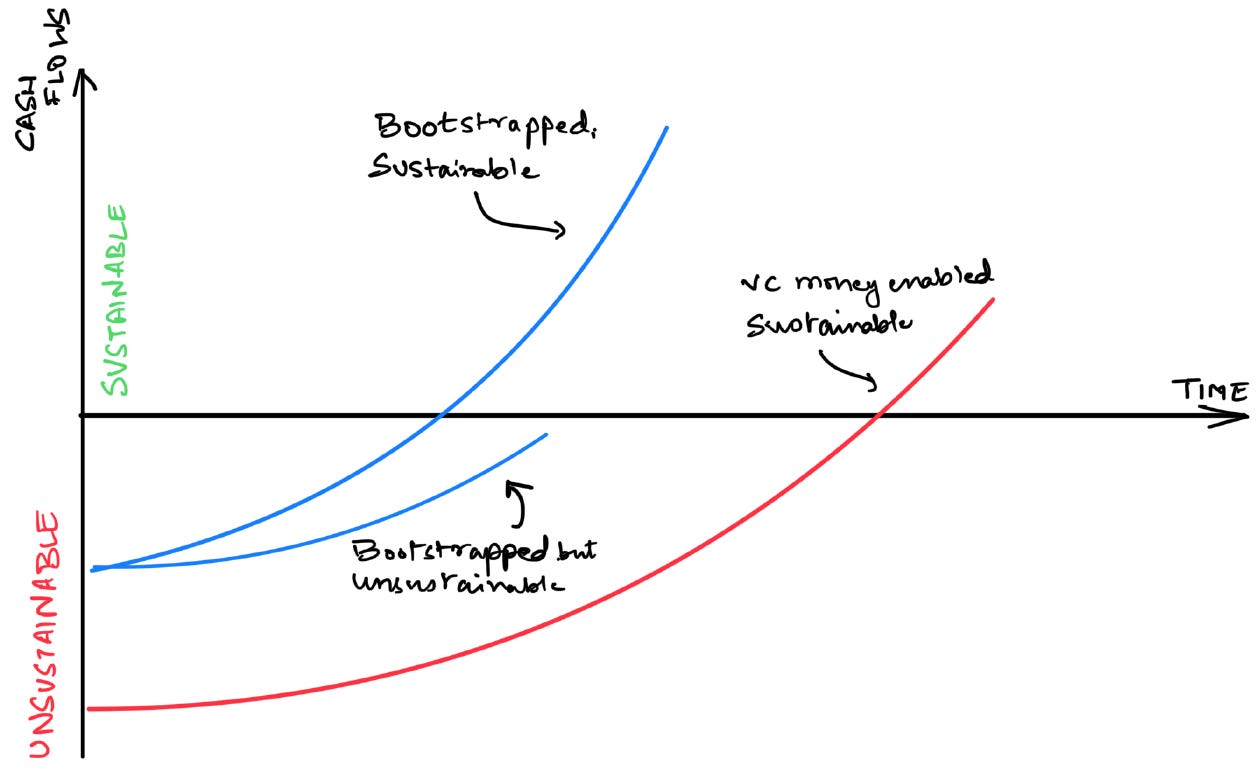

Venture Capital’s role is to provide high-risk capital to experiment. To provide a source of funding that is capable of staying the course even when the business is likely to remain unsustainable for longer than what the rest of the market is willing to bear.

Think of some of the most highly valued companies on the planet. Apple, Google, Amazon, FB and so on - they are all companies that operated unsustainably for quite a while before they became cash flow generating machines. To carry on with the same context, the same graph with VC funding will look like this:

This is a good thing.

The luxury and leeway of being able to throw a bunch of things on a wall and see what sticks has been critical towards setting up fundamental transformations of the world. Think of where we would be without Intel and Amazon.

However, much like anything else, too much of a good thing can be extremely harmful. This is particularly true of Capital. Any number of highly valued business funded with hundreds of millions of VC dollars are yet to turn a profit (or even show that they can some day). Being a beneficiary of huge amounts of risk capital allows companies to hide the less-than-sustainable aspects of their businesses.

Uber is a great example of this. Since its listing 6 or so years ago, Uber has lost $30bn in market cap1. In a company-wide email, the CEO Dara K made an almost stunning call to action to his staff:

“This next period will be different, and it will require a different approach…

We have to make sure our unit economics work before we go big.”

For a 10 year old company - I don’t have words.

The trouble is, Uber has been very consistent in one claim - that it will reach profitability when it hits scale. Now, Uber currently operates in 70+ countries, ~11,000 cities, has had about 120mn MAUs and ~7 billion trips in 2022. If this is not scale already, I don’t know where from this elusive scale will be achieved.

You know who I think of when I think of Uber and It’s elusive scale? These guys:

Gravity is a fundamental law of the universe:

Between 2012 and 2022, something crazy happened. VC investments exploded from ~20bn to ~350bn. That is an increase of 17x. Now, a lot of this has to do with the perverse incentives in a cash rich environment.

VC business model is about aggregating AUM and collecting fee. Sooner you deploy the cash, sooner you can raise more AUM and collect more fees. This tends to send VCs looking actively for cash hungry startups that can burn unholy amounts of cash. Pointless acquisitions, crazy S&M spends and worse, startups selling to other startups (thus propping valuations like a proverbial house of cards).

Now, think of companies that have been built in a capital rich environment. VC money was thrown at such crazy speed in a FOMO induced delirium that burn rate became an indicator of progress. Who came up with that?

To be fair, all businesses burn cash in pursuit of becoming a future economic engine that throws out more cash than it takes in. It takes time to get there. But generally, there is a point at which the forbearance for loss-making ends.

Plentiful capital has extended this forbearance to the point of ridiculousness. VC money today is less risk capital and more akin to a subsidy. So, the same graph now looks like this:

Now that the subsidy party is over. Guess what happens? Gravity is about to smack these businesses in the middle of their forehead.

To quote Buffett:

“…only when the tide goes out do you learn who has been swimming naked.”

VCs, FOMO and Implosions

You know what happens when too much capital chases too few good companies? Valuations become insane. Which makes even otherwise mediocre businesses look extremely attractive.

Let’s look at the enterprise SaaS market. in early 2021, the average enterprise SaaS company was trading at ~40x FTM revenues. This became the greatest driver of FOMO I have seen in recent history. Every tom, dick and harry startup with single digit million$ ARR2 was worth tens or hundreds of millions at the time and in time, the next $100bn company.

However twisted, the internal logic for this pattern of thinking is consistent - even if we miss by a few billion $ - who cares about entering a $5mn ARR company at $2bn when it can be worth $50, 60, 70bn? It is an absolute no-brainer.

And so, capital flooded in. More money meant that the fight for customers effectively became an arms race. People assumed the TAMs were unlimited even as the distribution channels became noisier and noisier. Ultimate beneficiaries - FB, Google, AWS.

As early as 2013, Paul Graham was telling founders to be extremely circumspect about their need to raise money:

“Don't raise money unless you want it and it wants you.

Such a high proportion of successful startups raise money that it might seem fundraising is one of the defining qualities of a startup. Actually it isn't. Rapid growth is what makes a company a startup. Most companies in a position to grow rapidly find that (a) taking outside money helps them grow faster, and (b) their growth potential makes it easy to attract such money. It's so common for both (a) and (b) to be true of a successful startup that practically all do raise outside money. But there may be cases where a startup either wouldn't want to grow faster, or outside money wouldn't help them to, and if you're one of them, don't raise money.

The other time not to raise money is when you won't be able to. If you try to raise money before you can convince investors, you'll not only waste your time, but also burn your reputation with those investors.”

Sage advice. Mostly ignored.

In 2016, Bill Gurley was trying hard to explain the dangers of unlimited capital availability to startups:

“Today’s Unicorn entrepreneur has been trained in an environment that may look radically different from what lies ahead. Here is the historic perspective. Money has been easy to raise. The market favors growth over profits. Competition also has access to capital. So, raise as much as you can as fast as you can, and be super-ambitious. Take as much market share as you can.

Never in the history of venture capital have early stage startups had access to so much capital. Back in 1999, if a company raised $30mm before an IPO, that was considered a large historic raise. Today, private companies have raised 10x that amount and more. And consequently, the burn rates are 10x larger than they were back then. All of which creates a voraciously hungry Unicorn. One that needs lots and lots of capital (if it is to stay on the current trajectory).”

Take a moment here. Think deeply about what Paul and Bill are saying here. You are a startup which has raised hundreds of millions of $s. You have been hooked onto cash being mainlined into your veins. Your system now only works when it is taking in an almost never-ending amount of cash. Like a Drug Addict, your tolerance is increasing. You need more and more cash to feel the same high. And there is no VC-addicts-anonymous with a 12 step program. These are the Mount Rushmore guys of Venture Capital. They were warning us about the distortions and risks of unfettered pools of Capital. No one listened.

And now, we are in 2023 and high interest rates have rolled around. Funding winter has set in. There isn’t as much cash available as capital flees to (relatively) safer yield products. Sink or Swim. Most will sink.

VC is a pass the parcel business as it is practiced today. You know, some of the most iconic phrases - “growth at all costs”, “move fast and break things”, “blitzscaling” - are all applications of the greater fool theory. Who gives a crap if Uber has lost $30bn in market cap. Early VCs made money when it went IPO as they passed on the parcel. Not our problem anymore. Can you blame them? It was ticking after all.

Concluding:

I must sound to you like a hopeless pessimist. I am not. I am as optimistic as they come. I believe that new is always better, that the future will be a better place. At the same time, I have a brain and I insist on using it instead of sticking my head in the sand like an Ostrich and pretending all is well.

VC exists because it is needed. Startups exist because they foster innovation. Experimentation exists because a few crazy people always will think of what could be. I do not want less of any of it. But I would like to see more thinking about second and third order effects instead of a shoot-first-ask-questions-later approach. Circumspection is a friend, not an enemy.

No one person and no single firm is to blame. Where we are today is a function of the environment, human nature, herd mentality. People played the game as best as they could with the cards they had. Fair.

I will take a leaf from The Newsroom here. The first step in solving a problem is realizing you have one. Here it is then:

“Massive amounts of capital deployed at breakneck speeds have distorted the way businesses are built. They are now indexed on consuming capital instead of durability. Building durable businesses is fast becoming a lost art.”

Housekeeping:

As always, I look forward to hearing from you. If you liked this post, pls feel free to share this or subscribe to this newsletter using the links below. While I have been tardy of late, I try to write a 1000-2000 word essay once every 4 weeks or so.

Or just the 2020 GDP of Estonia, Latvia or Bahrain. Take your pick.

quality of said ARR be damned.